Your payments team is spending time on work that should not exist. They're reconciling transactions across providers, switching traffic during outages, pulling reports from five dashboards, and chasing approvals. That is not a headcount problem. It is an architecture problem.

The stakes are real. Failed payments and poor operations cost the global economy an estimated $118.5B in 2020 alone, and those costs compound as volumes grow. Despite this, many organizations still rely on manual, file-based processes and paper checks. In fact, a large share of businesses continue to run legacy payment workflows long after the breakpoints are obvious.

Automation is no longer a "nice to have." It is a strategic move for finance teams and payments leaders who need to cut operational drag, stabilize revenue, and scale globally. When you automate payment reconciliation, you reduce errors and speed up the process from approval to settlement, while giving leadership real-time visibility into cash flow and risk.

From payment orchestration to automated routing, modern infrastructure transforms how teams handle transactions at scale.

What we hear from the field

"We can't get daily information without manual dashboard work – filters break on updates."

Global QSR brand

"Manual reconciliation is a tax on the team."

Travel marketplace

"Response times and reporting are too slow. We need real-time data."

Mobility brand

This article quantifies the real cost of manual payment operations and shows how smart teams automate. It also outlines how Yuno helps CFOs, Heads of Payments, CTOs, and Product leaders move faster with fewer manual tasks.

The True Cost of Manual Payment Operations

Manual payment work hides in calendars and spreadsheets. It looks small until you measure it. Then it becomes clear: it's a drag on margin, cash flow, and growth.

Time and labor inefficiency

Manual steps consume hours every day. Teams key in payment data, reconcile settlements line by line, validate invoices, and chase approvals. Accounts payable staff alone can spend close to one-third of their time fielding questions or hunting documents instead of moving work forward. That load spills across finance teams, payments operations, risk, and product. Smart teams are moving to unified payment platforms that consolidate these workflows into a single operational view.

The impact is tangible.

Teams spend hours on manual data entry and bank reconciliations every day. The work feels "urgent," but it does not drive revenue. Manual reconciliation tasks pile up, especially during high-volume periods like month-end close.

Repetition breeds burnout. High-skill staff end up doing low-leverage tasks. As a result, morale drops and turnover rises.

Strategic work stalls. When finance teams spend cycles fixing financial data, they delay projects that lift conversion, reduce fraud, or enable new markets.

Error-prone processes

Humans make mistakes. And manual payment workflows magnify them.

Duplicate payments, typos, and mismatched records are common in manual invoice flows. Studies report error rates of 1-2% for hand-processed invoices. More than 60% of invoice errors trace back to manual data entry.

These aren't just spreadsheet problems. Errors trigger late payments and disputes. Each cycle spent untangling a misapplied charge or double-paid vendor adds cost and strains relationships. When a payment error reaches a supplier, expect rework, potential penalties, and more manual verification downstream – a compounding cost that rarely shows up in dashboards until quarter-end.

The reconciliation bottleneck: manual reconciliation is particularly error-prone when dealing with:

- Partial payments split across multiple transactions

- Multiple payment methods used by the same customer

- High-volume transaction periods that overwhelm spreadsheet-based tracking

- Cross-border payments with currency conversions

Without real-time transaction matching, finance teams struggle to identify discrepancies before they cascade into larger problems. Advanced payment routing strategies can also reduce failed transactions at the source, preventing reconciliation issues downstream.

Security and compliance risks

Manual steps increase risk exposure across your payment operations.

Paper checks, unencrypted files, and ad hoc processes are fertile ground for fraud. Businesses face higher exposure to payment fraud when approvals and controls are not digital and auditable.

Audit trails suffer. Without a system that logs every action, investigations take time and distract leaders from higher-impact work. Manual processes make it nearly impossible to maintain comprehensive audit trails that meet regulatory and auditor requirements.

Compliance gaps create reputational and financial risk. Manual handoffs can break policy, violate segregation of duties, or miss emerging regulatory requirements. When your bank account activity isn't automatically reconciled with your payment processor data, you create blind spots that auditors will find.

How Manual Payment Processes Impact Business Growth

Manual operations do not just waste hours. They slow cash flow, cloud decisions, and cap scale.

Cash flow delays and inefficiencies

Manual payment steps lengthen cycle times from approval to settlement. Delays obstruct liquidity and forecasting. Teams also miss early-payment discounts because paperwork and approvals lag behind business needs.

Even when teams compress timelines, the variability introduced by manual effort makes it harder to manage working capital. Automated systems with real-time reconciliation reduce that variance and shorten the path to cleared funds. When you lack real-time data, you're managing your business with yesterday's information. Learn more about optimizing payment performance to accelerate settlement times and improve working capital management.

The working capital trap: without real-time visibility into which payments have cleared your bank account and which are still pending, CFOs struggle to optimize cash positioning. This is especially painful during high-volume periods when manual reconciliation can take days to complete.

Limited transparency and control

Leaders need real-time visibility. Manual processes offer only periodic snapshots.

Tracking payment status across banks, acquirers, and alternative payment methods becomes a scavenger hunt without a unified operational view. Different providers use different reporting formats. Manual reconciliation across these systems is tedious and error-prone.

Reporting lags. Decisions rely on stale financial data, especially when dashboards are spread across providers and exports require manual normalization.

The result: slow answers to urgent questions about cash position, provider performance, or regional anomalies. When your team can't quickly identify discrepancies between what your payment processor reports and what hits your bank account, you're flying blind. This is why payment analytics and reporting have become critical infrastructure for modern finance teams.

Reduced scalability

Manual workflows buckle under growth.

As transaction volumes climb, handoffs multiply. Each exception creates additional manual effort and introduces new opportunities for delays or errors. Payment reconciliation that took two hours per week on 1,000 transactions per month could require a full-time headcount at 50,000 transactions.

Expansion adds complexity. New markets, payment methods, and providers mean new files, new rules, and more reconciliations – unless you automate payment reconciliation processes. Scaling globally requires more than automation. It demands smart payment localization and regional optimization

Manual complexity grows nonlinearly. That is the point where teams pause expansion to "shore up ops" – and competitors move first. High-performing finance teams recognize that manual reconciliation becomes a bottleneck to growth.

Benefits of Automating Payment Operations

Automation is not just faster. It is safer, more cost-effective, and easier to control.

Enhanced efficiency and cost savings

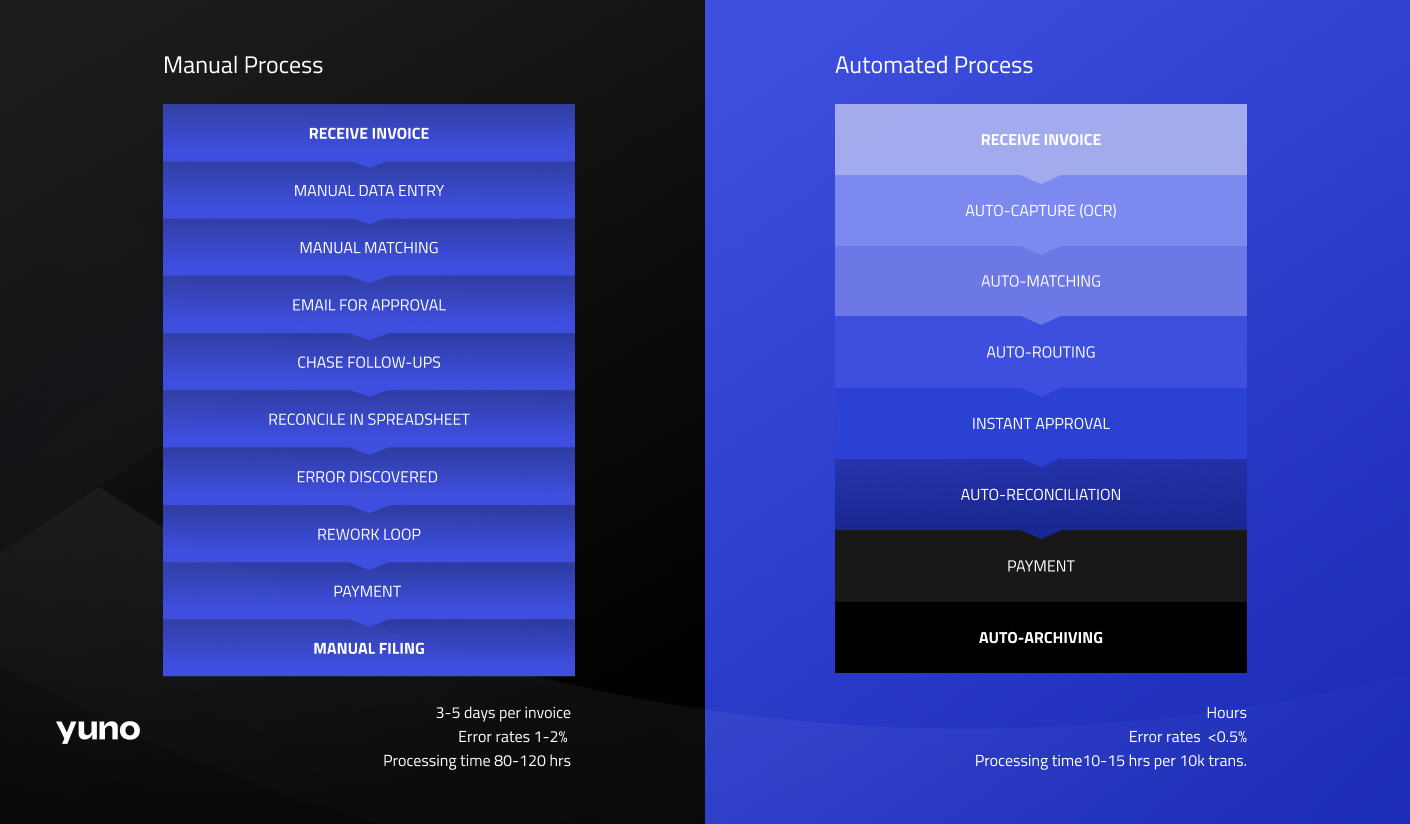

Automation slashes processing time. Systems capture, validate, route, approve, and reconcile far faster than any manual flow. The cost delta is wide: manual invoice processing often runs $15-$40 per invoice; automation can bring it down to a few dollars in many scenarios.

That efficiency frees headcount for strategic work – fraud models, pricing, new products – instead of administrative churn. When you automate payment reconciliation, your finance teams can focus on analysis instead of data entry.

Real-world impact: teams report a 70-80% reduction in payment-matching errors after implementing automated reconciliation. Manual data entry, which once took 20 hours per week, has shrunk to 2-3 hours of exception handling.

Improved accuracy and security

Automation reduces errors at the source and hardens security.

Systems validate financial data and prevent duplicates before it is posted to the ledger. This removes the bulk of manual-entry mistakes and the rework they cause. Automated bank reconciliation catches mismatches in hours, not days.

Security improves with tokenization, encryption, and role-based controls built into the payment flow. This reduces exposure to fraud and data leakage. Comprehensive audit trails are generated automatically, documenting every action taken on every payment.

Real-time transaction matching ensures that discrepancies are identified immediately, not during month-end close. Systems can automatically match incoming payments to invoices, flag partial payments for review, and reconcile across multiple payment methods simultaneously.

Better visibility and compliance

Automation centralizes logs, events, and reports across your entire payment ecosystem.

Real-time reconciliation and analytics give leaders a live view of approvals, declines, retries, settlements, and disputes. This enables faster corrective action. Finance teams gain real-time visibility into cash flow without waiting for batch reports or manual data pulls.

Audit-ready records and consistent controls simplify compliance and reduce audit and investigation costs. When regulators request documentation, you can produce complete audit trails in minutes rather than days.

Cross-functional benefits: when your payment reconciliation is automated, sales teams get faster commission calculations. Customer service can instantly verify payment status. Treasury can optimize cash positioning with real-time data.

What the shift looks like in numbers (illustrative)

Below is a simple view of how automation changes the operational math for a mid-size merchant. Figures are placeholders to show magnitude; your results will vary by mix, markets, and team structure.

Metric (monthly) Manual baseline With automation What changes Sources Processing cost per invoice/payment task $15–$40 ~$2–$5 Automated capture, approvals, and settlement reduce per-unit cost Airwallex Invoice/payment data errors 1–2% <0.5% Validation and dedupe at ingestion Sensetask Ops hours on reconciliation/reporting High (hundreds) Low (tens) Unified data, auto-matching, real-time dashboards Industry standard Fraud exposure from manual steps Elevated Reduced Encryption, tokenization, controlled access VoPay Missed early-payment discounts Frequent Rare Faster cycle times and programmable approvals Airwallex Time to identify discrepancies Days Hours or real-time Automated matching and alerts Industry standard Manual effort per 10,000 transactions 80-120 hours 10-15 hours Reduced manual data entry and exception handling Composite

How Yuno Automates the Heavy Lift

Yuno unifies global payments. One platform, full control. We help teams cut manual effort, lift performance, and scale faster – without adding complexity.

- Global reach – Process payments in 40+ countries with local relevance.

- Operational control – One API, 200+ integrations. Launch new markets in days, not months.

- Performance optimization – Intelligent routing that lifts approval rates. Merchants using Yuno see an average lift of around 8% in approval rates.

- Security and stability – PCI‑DSS Level 1 certified. 99.99% uptime.

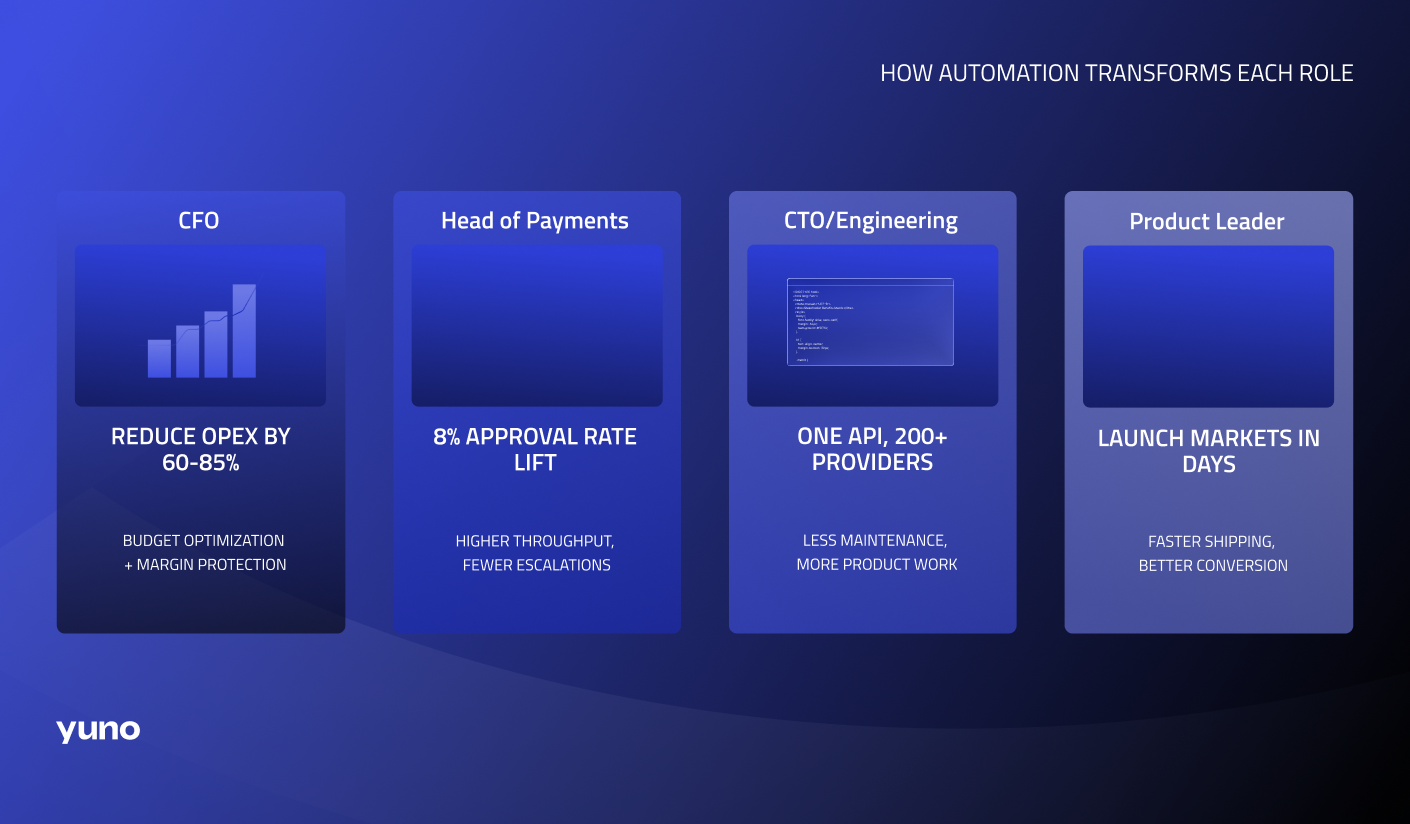

For CFOs: Reduce OpEx and protect margin

1. Lower unit costs by automating payment tasks that consume headcount today. Automate payment reconciliation to free your finance teams from manual data entry.

2. Redeploy talent from bank reconciliation and reporting to cash flow forecasting and margin programs.

3. Gain a single operational view for settlements, fees, and provider performance – by market and method – with real-time data to inform pricing and budgeting.

Result: You free budget and improve predictability, while reducing the risk of quarter-end surprises. Real-time visibility means you always know your cash position.

For Heads of Payments: Fewer tickets, more throughput

1. Route across 200+ providers from one API. Yuno's orchestration platform adapts traffic by market and method to lift approvals.

2. Automate failover and retries. When a provider degrades, failover happens in rules, not war rooms.

3. Centralize reporting and alerts. No more toggling across dashboards to find what broke and where. Track performance across multiple payment methods in a single interface.

Result: Your team handles high volume with a smaller queue of manual issues. Reduced errors mean fewer customer service escalations.

For CTOs and Engineering: One integration, less maintenance

1. Replace bespoke payment plumbing with orchestration. One API, consistent webhooks, unified schemas.

2. Cut integration debt. Add new payment methods and providers without new builds.

3. Reduce incident load with stable infrastructure and clear observability. Built-in audit trails mean faster troubleshooting.

Result: Fewer sprints spent on providers. More time for the core product.

For Product Leaders: Faster launches, better conversions

1. Enter new markets in days. Turn on local payment methods with the coverage you need.

2. Lift conversion with adaptive routing and retries tuned to regional performance.

3. Use granular analytics to optimize checkout and post‑payment flows. Real time transaction matching helps you understand exactly where friction occurs.

Result: You ship faster and convert more traffic – with fewer manual detours.

Steps to Transition from Manual to Automated Payments

You can move fast without losing control. Here is a proven path.

Assess your process and pinpoint automation wins

Map the workflow end-to-end. Identify where time and errors cluster: data capture, approvals, provider switching, bank reconciliation, and dispute handling.

Quantify the drag. Estimate hours lost, error rates, and impact on discounts and disputes. Start where the payoff is biggest – often invoice intake, approval routing, and payment reconciliation.

Common pain points to evaluate:

- How long does manual reconciliation take during high-volume periods?

- How many payment methods do you support, and how do you reconcile each?

- Can you identify discrepancies in real time, or only during batch processing?

- Do you have real-time visibility into your bank account vs. payment processor balances?

- How much manual effort goes into creating audit trails for compliance?

Transition tip: ask, "What would we stop doing if the system did it?" That question surfaces quick wins.

Choose the right payment automation solution

Look for deep integrations, strong security, and global scale. You want to plug into providers and payment methods across regions without bespoke builds.

Demand real-time reconciliation, role-based access, and audit trails. Compliance and control should be built in, not bolted on. The system should automatically match transactions, flag partial payments, and identify discrepancies without manual intervention.

Pilot before you commit. Run a controlled test across a subset of markets or methods to validate performance, reliability, and reporting.

Evaluation checklist:

- Can we route traffic dynamically by currency, BIN, issuer, and provider health?

- Do we get a single source of truth for approvals, declines, fees, and settlements?

- How fast can we add a new provider or payment method in a priority market?

- Does the platform support real-time transaction matching across all our providers?

- Can we automate bank reconciliation without manual file uploads?

- Are comprehensive audit trails generated automatically?

- Does the system handle partial payments and complex matching scenarios?

For teams evaluating solutions, our guide on selecting a payment orchestration platform covers the technical and operational criteria that matter most.

Implement and optimize

Train your team. Show how workflows change and where they will save time. Clarify roles and approvals in the new model. Finance teams will shift from manual data entry to exception handling and analysis.

Measure and iterate. Track approval lift, reduced errors, ops hours saved, and time to market. Tune routing and retries based on real-time data. Automation is not set‑and‑forget – it improves with feedback.

Timeline expectations: Most teams can implement core automation in weeks, with broader rollout over a few months, depending on scope and regions. Start with your highest volume payment methods or most error-prone processes for quick wins.

Conclusion: Manual payment work is an avoidable tax

Manual payment operations drain time, create errors, and raise risk. They slow cash flow, cloud decisions, and cap growth. When you automate payment reconciliation, you flip the script – lower unit costs, fewer errors, stronger controls, and better conversion. The result is agility and scale.

Yuno makes this shift practical. We unify global payments with one platform – 200+ integrations, intelligent routing, real time reconciliation, and enterprise‑grade security. Teams often see approval lifts and measurable reductions in manual effort within weeks.

Let's explore what this looks like for you.

FAQ

What are the main risks of continuing manual payments?

Manual payments increase error rates, increase exposure to fraud, and slow cycle times. All of that raises costs and complicates compliance. Studies tie most invoice errors to manual data entry, and manual methods are more vulnerable to payment fraud and data leakage. Additionally, manual reconciliation makes it difficult to quickly identify discrepancies, creating cash flow blind spots and audit trail gaps.

How long does it typically take to automate payment reconciliation processes?

It varies by complexity and markets. Many teams deploy core automation in a few weeks and expand over a few months. Pilots help validate performance before full rollout. Start with high-volume payment methods or the most error-prone processes for the fastest ROI.

Is automation suitable for small businesses?

Yes. Automation scales. Even small teams benefit from faster processing, reduced errors, and stronger controls. The cost per task often drops from tens of dollars to just a few, which adds up quickly as volumes grow. Real-time visibility and automated bank reconciliation are valuable whether you process 100 or 100,000 transactions per month.

How does automated reconciliation handle partial payments and multiple payment methods?

Modern payment automation platforms use real-time transaction matching that can handle complex scenarios. This includes partial payments, split tenders, refunds, and multiple payment methods per transaction. The system automatically matches incoming funds to invoices, flags exceptions for review, and maintains complete audit trails across all payment methods.

Will automation eliminate the need for finance teams?

No. Automation eliminates manual data entry and repetitive reconciliation tasks. This allows finance teams to focus on higher-value work, such as cash flow analysis, financial planning, fraud prevention, and strategic decision-making. Teams typically redeploy saved hours to projects that drive revenue and reduce risk, rather than to headcount reduction.

What's the difference between payment orchestration and payment automation?

Payment automation handles repetitive tasks like data entry and reconciliation. Payment orchestration goes further. It intelligently routes transactions across multiple providers, manages failovers, and optimizes approvals in real time. Orchestration includes automation, but adds strategic control and performance optimization.