Merchants sit on a river of data. Every day, millions of payment transactions (across cards, wallets, bank transfers, and alternative payment methods) capture customer intent, friction, and revenue signals. When teams start analyzing payments with structured payment metrics instead of scattered spreadsheets, they uncover clear paths to growth. But most organizations still depend on siloed exports, incomplete transaction data, and dashboards that don’t tell the whole story.

This is where payment analytics becomes a strategic advantage. It converts unstructured payments data into visibility, action, and predictable results. With stronger insight into transaction amounts, payment types, country behavior, and accepted payment flows, global merchants can improve performance across their entire payment processing journey.

Below, we break down 5 practical ways high-performing merchants use payment analytics to:

- Boost authorization

- Reduce chargeback rates and fraud exposure

- Strengthen strong customer authentication (SCA)

- Improve checkout experiences by market

- Act on issues instantly through real-time data

Let’s start with why this matters.

1. The Untapped Power of Payments Data

Acquisition gets attention. But the quiet driver of margin (your payment performance) shapes everything from customer lifetime value to your ability to scale globally.

Across industries, 5-20% of attempted transactions fail. In subscription businesses, involuntary churn can reach 40% of total churn. Behind these losses are avoidable gaps in issuer logic, routing, latency, risk rules, and authentication friction.

Where teams get stuck

Blind spots in payment processing

You see what failed, but not why. A missing view of issuer behavior, risk flags, or payment gateway availability leaves teams guessing.

Fragmented data

Multiple processors, multiple markets – none aligned. Analysts spend hours stitching transaction data into something usable.

Slow analysis

Teams compare transaction amounts, APM performance, and credit cards versus debit card flows manually. By the time the insight arrives, the moment to act has passed.

No predictive view

Most dashboards explain yesterday. Few highlight emerging changes in customer behavior, online payments conversion, or fraud patterns.

2. The Business Impact – Revenue, Efficiency, and Better Experiences

When analytics shifts from reporting to directing action, merchant performance changes quickly.

Higher authorization rates

Tracking issuer trends, tokenization behavior, SCA outcomes, and routing drivers leads to measurable improvement. When merchants connect these insights to automated decisions, global approval rates rise.

Lower operational waste

Unified data reduces reconciliation time, dispute overhead, and manual fraud review. Support teams resolve issues faster because they finally see where payment transactions break down.

Smarter marketing efforts

Payments reveal more than revenue. Frequency, preferred payment types, and average transaction amounts help refine marketing efforts and predict future value.

Faster global expansion

What works for credit cards in Mexico is different from debit card behavior in Brazil. Analytics improves local strategy before you enter a market.

Better customer experiences

Less friction at checkout. More successful payments. Better mobile performance. When payments flow, everything else feels smoother.

3. What High-Performing Merchants Track

Top merchants go beyond volume. They track signals that reveal opportunities.

Authorization rate

Break it down by issuer, BIN, network, method, region, and SCA step-up.

Curious about how networks evaluate approvals? Visa’s merchant resource library provides guidance that helps merchants benchmark their authorization strategy.

Decline codes

Normalized decline codes expose meaningful patterns.

Chargeback rates

Monitor reason codes, recurring SKUs, and regional trends.

Fraud indicators

Velocity rules, device fingerprints, behavior patterns, and routing anomalies.

PayPal’s risk management tools and guide to chargebacks offer simple explanations of dispute and fraud patterns – check them out.

Transaction success ratio

The percentage of payment processing volume that clears end-to-end without intervention.

Refund and return ratios

Patterns linked to dissatisfaction or churn signals.

Payment flow timing

Latency across processors, gateways, and internal systems – a major driver of mobile conversion.

Cost per payment

Processing fees, FX spreads, dispute costs, and fraud losses.

Real-time data

Your ability to spot issues as they happen, not hours later.

4. 5 Ways Merchants Use Payment Analytics to Drive Revenue

These are the core use cases that consistently move the needle.

Way 1: Pinpoint the Root Cause of Declines

A merchant sees a sudden approval drop in Brazil. Analytics reveal elevated issuer timeouts on one acquirer.

- Action – Traffic shifts instantly to a healthier route

- Impact – Approval rates recover with no engineering work

Analytics replaces guesswork with precision.

Tools like the Stripe payments analytics documentation show how processors expose decline codes, authentication outcomes, and issuer behavior so teams can troubleshoot issues quickly.

Way 2: Reduce Chargebacks With Targeted Interventions

A spike in online payments chargebacks usually isn’t random. Analytics highlight patterns in region, device, quantity, and transaction amounts.

- Action – Adaptive SCA, clearer checkout messaging, smarter 3DS routing

- Impact – Lower chargeback rates and fewer false positives

Better insight leads to cleaner recovery strategies.

If you want a shopper-friendly explanation of PSD2 friction, Klarna’s explanation of PSD2 and strong customer authentication is a good example of how providers communicate these extra steps.

Way 3: Localize Checkout Experiences by Market

Every region behaves differently:

- Mexico – heavy reliance on debit card

- Brazil – local methods outperform cards in many verticals

- Europe – 3DS introduces friction that needs tuning

- US – credit cards dominate but behave differently by issuer

- Action – Local A/B tests through Yuno’s orchestration engine

- Impact – Higher conversion with no increase in fraud

Checkout adapts to regional expectations instead of forcing one global flow.

Way 4: Improve Subscription and Retry Performance

Subscription churn often ties to issuer logic, SCA requirements, and transaction amounts across retries.

The QuickBooks overview of recurring payments shows how recurring card and bank charges behave differently from one-off transactions – exactly the nuance your analytics should surface.

- Action – Adaptive retry strategies informed by historical success patterns

- Impact – Lower involuntary churn and higher recurring revenue

Analytics lets you adjust each retry to how the issuer actually behaves.

Way 5: Prevent Fraud Without Rejecting Good Customers

Machine-learning signals tied to payment transactions, device characteristics, and customer behavior detect risk early.

Platforms like Plaid Identity Verification documentation illustrate how combining identity, device, and behavior data reduces fraud while protecting conversion.

- Action – Fraud rules update in real time

- Impact – Lower fraud and fewer false declines

Fraud prevention becomes more precise and less disruptive.

5. The Data Challenges Merchants Still Face

Even advanced teams hit predictable roadblocks.

Fragmented payments data

Different processors, different file structures, inconsistent labelling.

Brex maintains resources for modern finance teams that highlight how fragmented financial and payment data slows down decision-making – the same issue merchants face in payments.

Inconsistent taxonomies

A “Do Not Honor” from one gateway becomes “Generic Decline” in another.

Limited visibility into issuer behavior

Without granular signals, optimization becomes trial and error.

Lagging dashboards

If insights arrive hours later, recovery is too slow.

Static routing rules

Rules don’t adapt to outages, SCA friction, or shifts in customer behavior.

These gaps slow teams down and hide revenue opportunities.

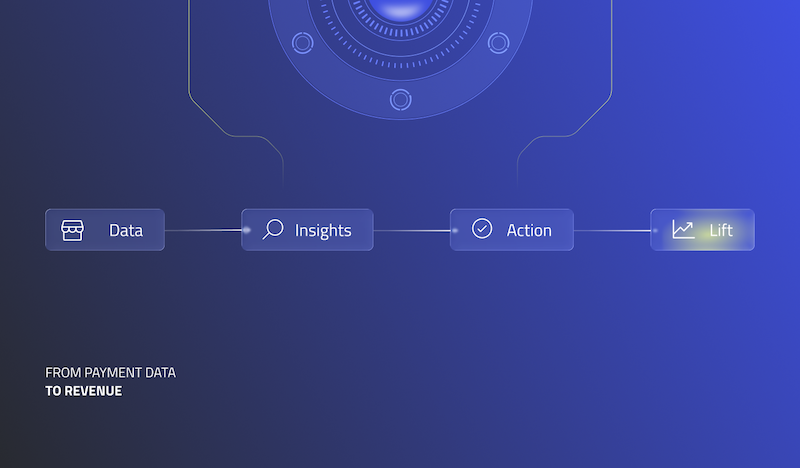

6. How Yuno Elevates Payment Analytics – From Insight to Action

Yuno unifies global payments data, enriches it, and connects it to orchestration.

1. Unified Data Across Providers

All processors, acquirers, gateways, and methods – normalized into one real-time layer.

2. Real-Time Decisioning

Failover routing, dynamic 3DS, adaptive retries, and fraud scoring update instantly based on live conditions.

This mirrors the broader movement toward automation in finance. For example, Ramp’s overview of finance automation highlights how real-time signals outperform delayed reporting in operational workflows.

3. Aida AI – Instant clarity in your payments dashboard

Yuno also brings intelligence straight into your workflow through Aida – our embedded payment operations agent. Aida gives teams fast, frictionless answers so they can act with confidence.

- Instant payment clarity. Ask Aida anything about a transaction. Decline reason, issuer behavior, authentication steps, and customer data. If it’s in the JSON, she surfaces it in seconds.

- Insights on demand. Describe the metric or comparison you want. Aida generates the chart and adds it to your custom Insights view.

- Routing by description. Tell Aida the logic you need, and she builds it. Fewer clicks, cleaner configs, no engineering queue.

One agent, multiple workflows, zero complexity. Aida turns analytics into action right where your team already works.

4. Advanced Analytics Tools

Teams can easily explore:

- Authorization and issuer trends

- Latency and routing bottlenecks

- SCA friction and step-up outcomes

- Payment gateway performance

- Fraud indicators and behavior anomalies

- Checkout drop-off patterns

- Marketing efforts tied to payment behavior

4. Operational Control

Finance teams get cleaner reconciliation. Risk teams get earlier alerts. Payments teams get clarity without manual stitching.

5. Proven Results

Across enterprise merchants, Yuno typically delivers:

- 3-8% lift in approval rates

- 20-40% reduction in involuntary churn

- 30-60% fewer manual operational tasks

- Faster entry into new markets

Analytics drives action, and action drives revenue.

7. The Future of Payment Analytics

The next era isn’t more dashboards – it’s adaptive intelligence.

Predictive analytics

Forecast declines, fraud spikes, and optimal routing choices.

Issuer–merchant collaboration

Shared insights reduce friction and unnecessary declines.

Contextual authentication

SCA adapts to the user’s risk level and history.

Checkout personalization

Different flows for different customers, informed by customer behavior and payment types.

Cross-provider intelligence

A unified view across the entire transaction chain, not one processor at a time.

At a macro level, Forbes’ analysis of how technology is reshaping the global payments landscape reinforces the same trend: payments are becoming more intelligent, integrated, and data-driven.

Yuno is building toward this future today.

8. How to Get Started

If you’re early:

- Consolidate your payments data

- Normalize decline codes

- Benchmark performance by method, issuer, and market

- Identify your largest leaks

- Test targeted routing or SCA improvements

- Share insights across product, risk, and ops teams

If you want to accelerate, Yuno can help.

Ready to Turn Payments Data Into Growth?

Payment analytics is no longer a reporting function – it’s a revenue engine.

With Yuno, global merchants gain the clarity, control, and real-time automation needed to:

- Capture more successful transactions

- Reduce friction

- Expand globally with confidence

- Strengthen fraud defenses

- Improve checkout experiences at scale

If you want a payment stack that adapts to every market, issuer, and customer in real time, we’d love to talk.

Let’s unlock your next revenue jump.