Payment routing is one of the most overlooked levers in modern payment infrastructure. Yet for U.S. merchants processing high volumes of online transactions, routing decisions directly affect approval rate, cost, and customer experience.

This guide explains the types of payment routing, how payment routing works inside a payments system, and which payment routing strategies help merchants reduce declines, recover failed payments, and scale global payments with confidence.

Why Payment Routing Matters in Modern Payments Systems

Every failed transaction is lost revenue.

Issuers apply stricter controls to online and cross border payments than to in-person transactions, even when fraud risk is low. As a result, card-not-present flows consistently show lower authorization rates, leading to more declining transactions in ecommerce and subscriptions.

Even small improvements matter. Recovering just a portion of false declines can lift accepted payments by 1-2% at scale, which translates to millions in incremental revenue for enterprise merchants.

Payment experience also impacts trust. Research shows that when payments fail, customers are far less likely to retry or return, especially on mobile checkout.

What Is Payment Routing?

Payment routing is the logic that determines how customer payments move through the payments system after checkout.

Routing decides:

- Which payment processor handles the transaction

- Which acquirer submits it to the card network

- How the request reaches the issuing bank

- Whether fallback logic is triggered after a failed payment

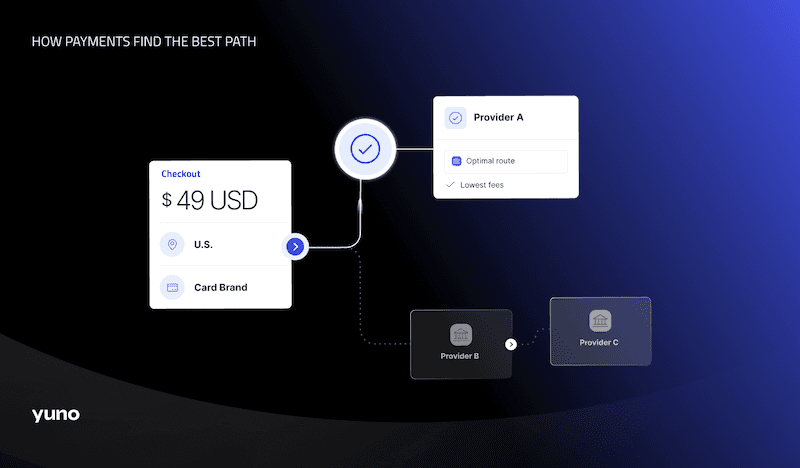

The goal is to route each payment transaction through the path most likely to result in an accepted payment, while balancing cost, speed, and risk.

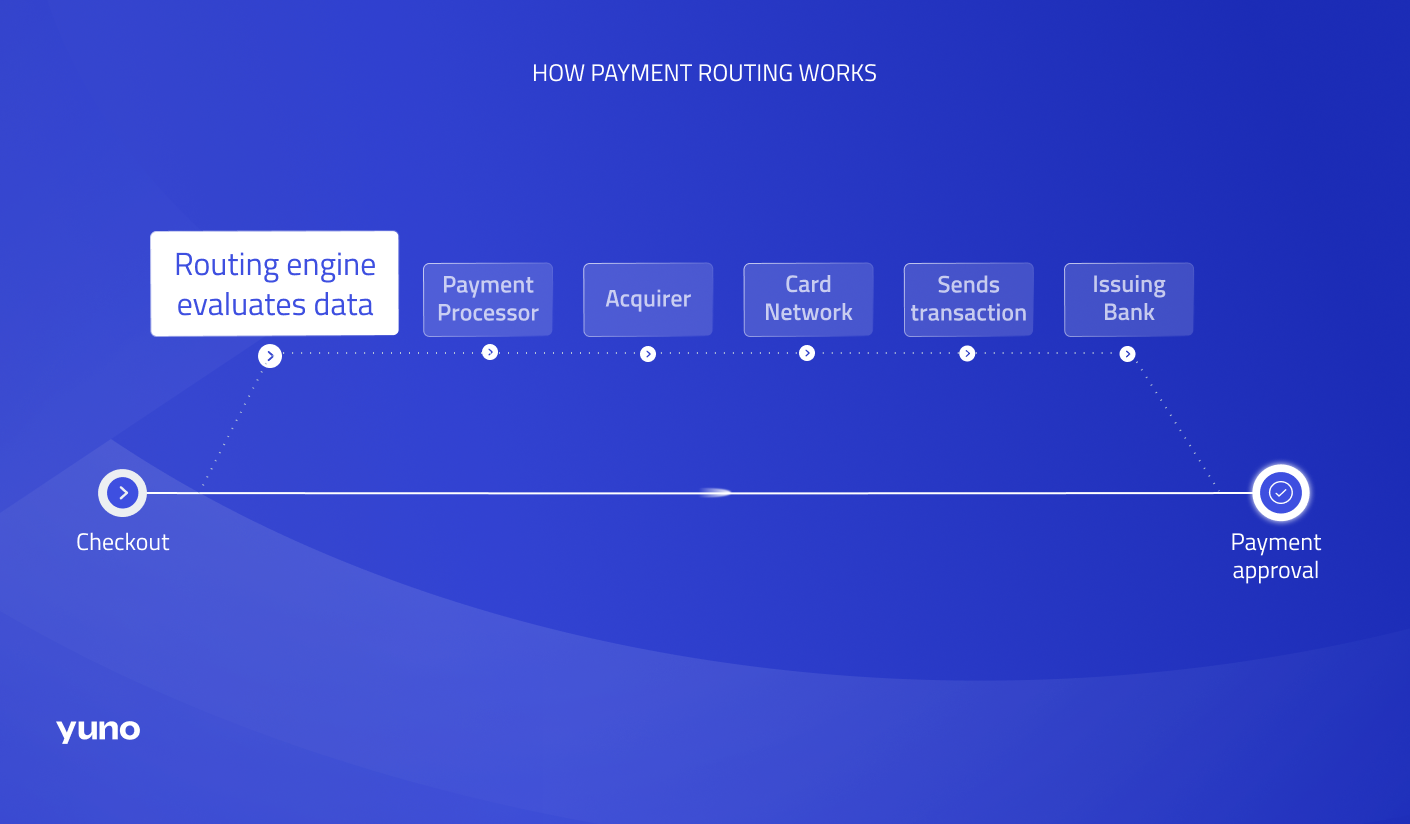

How Payment Routing Works

Understanding how payment routing works requires looking at the full transaction flow.

Layer Role in the Route System Checkout Captures customer payment details Routing engine Applies routing strategy Payment processor Routes transactions to acquirers Acquirer Submits authorization Card network Transfers request Issuing bank Approves or declines

Routing logic evaluates real-time signals such as card type, issuer behavior, geography, and provider performance. Adjusting how requests are formatted, routed, or retried can materially change issuer outcomes.

How payment routing works

Types of Payment Routing

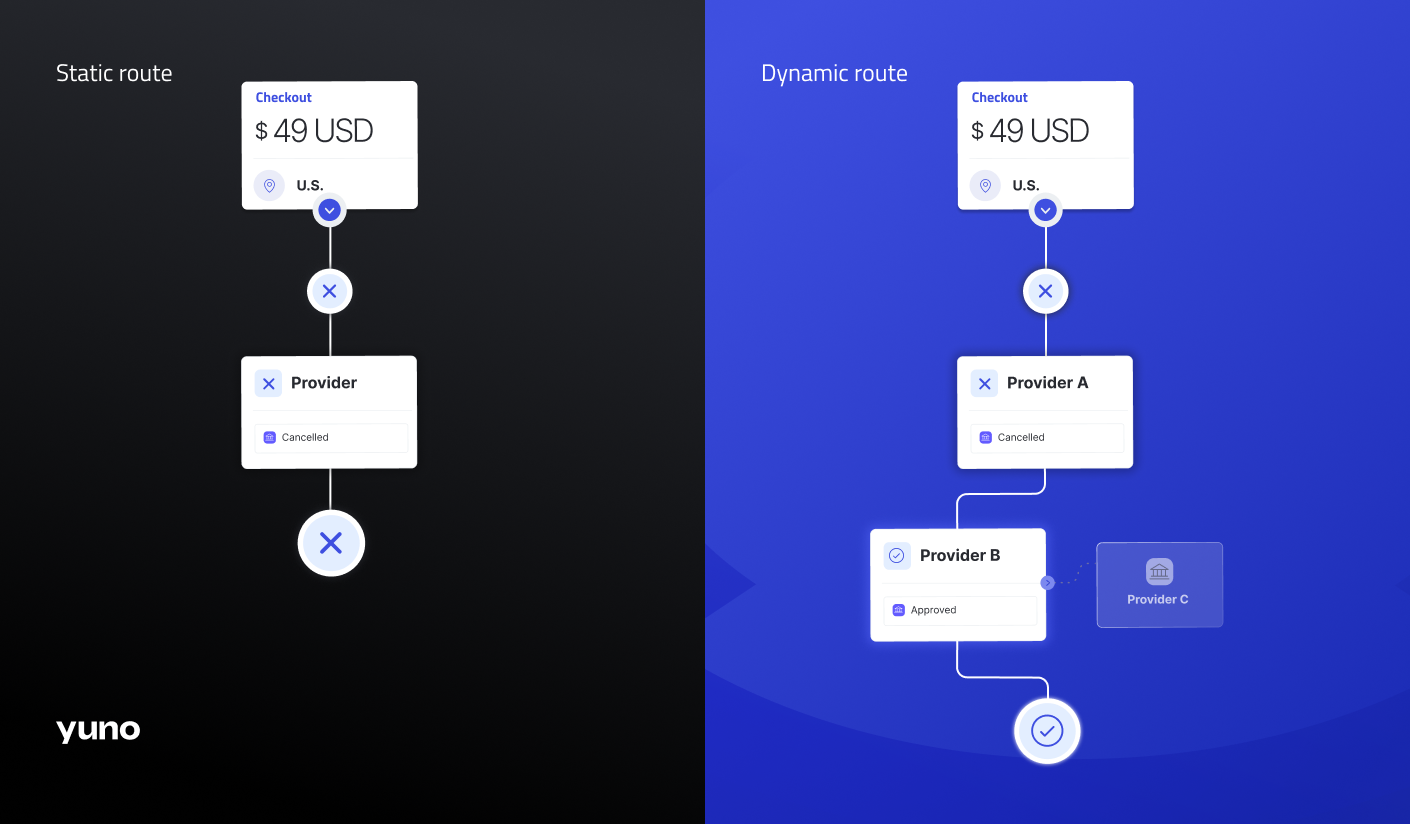

There are two primary types of payment routing: static routing and dynamic payment routing.

Static Routing (Direct Routing)

Static routing sends all payment transactions through one fixed path.

This route system does not adapt to:

- Credit or debit card differences

- Issuer preferences

- Domestic vs. cross border transaction logic

- Provider performance shifts

When Static Routing Is Used Scenario Why Single region Low complexity One currency Fewer variables Low volumes Limited optimization upside

Limitations of Static Routing Issue Impact No fallback More failed payments No issuer optimization Lower approval rate Provider outages Direct revenue loss

Issuer behavior varies significantly by geography and acquirer, which static routing cannot accommodate, leading to unnecessary declines.

Manual Routing (Static + Human Control)

Manual routing introduces people into a static routing model.

Teams update routing rules in dashboards or code after problems appear.

Where Manual Routing Fits

- Regulatory or compliance edge cases

- Temporary provider incidents

- Limited testing of new payment options

Tradeoffs Benefit Cost High control Slow response Custom rules Engineering overhead Short-term fixes Revenue lost during delays

Manual financial workflows struggle to scale in real-time environments, where payment failures need immediate response.

Dynamic Payment Routing (Smart / Intelligent)

Dynamic payment routing evaluates each transaction independently and routes it in real time.

This is also known as smart routing or intelligent payment routing.

Each payment is routed based on:

- Issuing bank behavior

- Card network performance

- Credit or debit card type

- Domestic vs. cross border payment logic

- Transaction type (one-time vs. recurring payment)

- Provider approval rate and latency

If the first attempt fails, the system automatically retries through a fallback path—recovering failed transactions without customer friction.

Many declines are not final. Soft declines can often be recovered by retrying through a different route or adjusting transaction data.

Comparison: Types of Payment Routing Routing Type How It Routes Transactions Best For Strengths Weaknesses Static routing One fixed path Simple setups Easy to launch High failed payment risk Manual routing Human-updated rules Edge cases Control Slow, costly Dynamic payment routing Real-time decisioning High volumes, global payments Higher approval rate, resilience Needs orchestration

Static route vs dynamic route

What Shapes an Effective Routing Strategy

Cost Optimization

Routing affects interchange, processor fees, and cross-border costs.

Cross border payments often fail or cost more when routed internationally instead of locally. Routing payments locally can materially improve acceptance and reduce fees in international payments.

Risk and Decline Management

Routing strategy plays a major role in how merchants reduce declines.

Not all declines indicate fraud. Many are issuer-driven and recoverable with better routing, retries, or provider selection.

This balance is especially important for recurring payments, where a single failed payment can trigger involuntary churn.

Business Model and Payment Mix

Routing performance varies by types of payments.

Why Routing Matters by Business Model Model Why Routing Matters Subscriptions Failed payment = churn Marketplaces Mixed risk profiles Cross-border ecommerce Issuer-local preferences Mobile checkout Low tolerance for failure

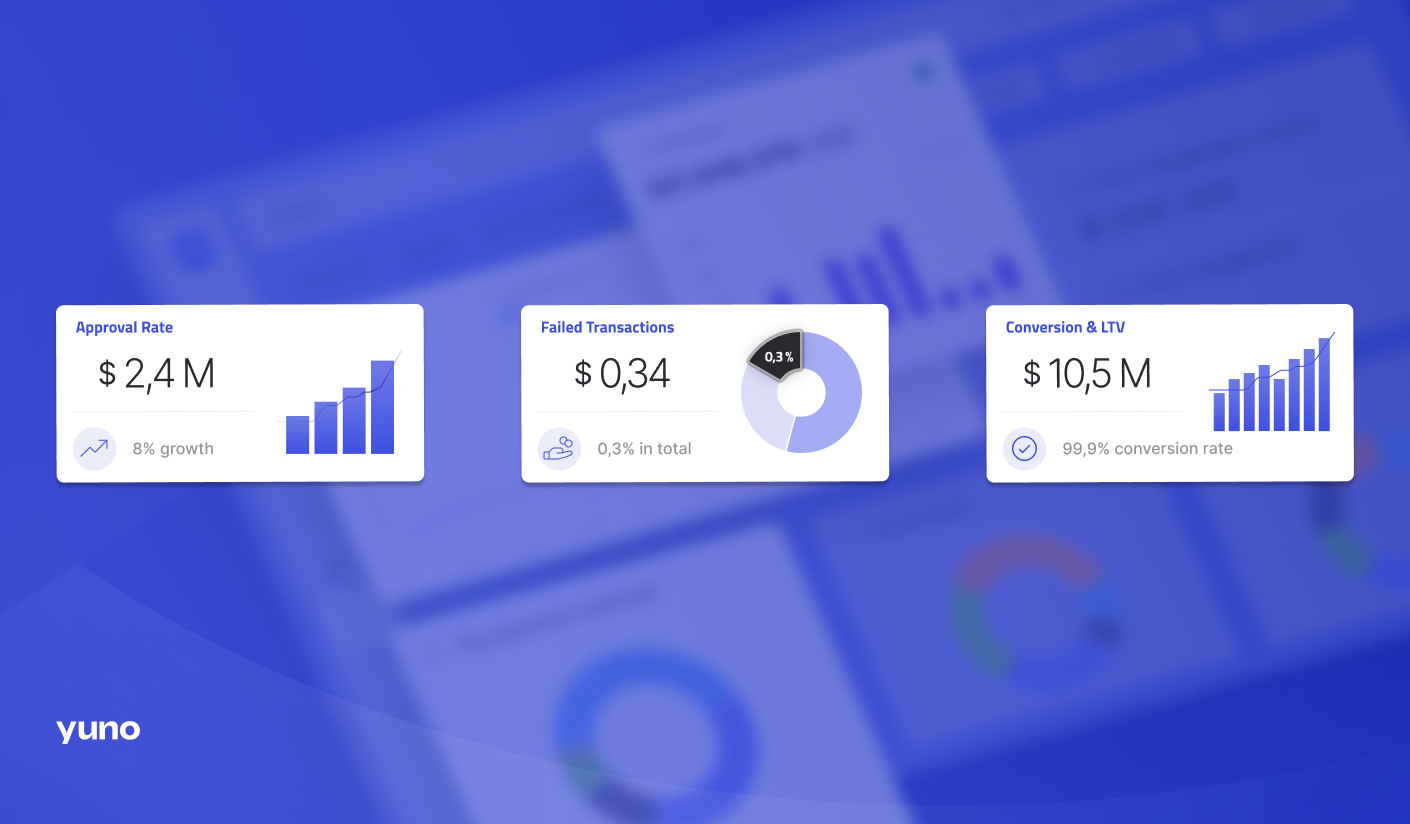

Benefits of Optimized Payment Routing

Benefits of Optimized Payment Routing Outcome Business Impact Higher approval and authorization rates Revenue lift Fewer failed transactions Higher conversion Lower processing costs Margin protection Better customer experience Higher LTV

Business Outcomes of Smart Routing

Key Takeaways

- Payment routing determines how transactions reach the issuing bank

- Static routing is simple but rigid

- Dynamic payment routing adapts in real time

- Smart routing helps reduce declines and recover failed payments

- Routing strategy is critical for global payments at scale

In modern payments systems, routing is not optional optimization. It is how merchants protect revenue, improve approval rates, and ensure customer payments succeed – across online transactions, recurring payments, and international markets.

The best payments don’t feel complex. They just work.