In today’s global e-commerce landscape, relying on a single acquiring bank can limit performance and increase risks. Merchants face varying approval rates by geography, frequent cross-border fees, and the possibility of downtime if their sole provider experiences technical issues. To address these challenges, many enterprises adopt a multi-acquirer strategy.

Managing payments with multiple acquirers is not just about adding redundancy—it is about creating a smarter, more resilient payments infrastructure that can scale with business growth. This guide explores why merchants pursue multi-acquirer setups, the challenges involved, and how payment orchestration simplifies the process while unlocking new revenue opportunities.

What does it mean to work with multiple acquirers?

When a merchant partners with multiple acquiring banks, they gain the ability to route transactions to different acquirers depending on region, card type, or performance. Instead of all transactions flowing through one channel, payments are distributed across providers.

For example:

- A U.S.-based merchant might work with a local acquirer for domestic card payments while using a European acquirer to optimize transactions in the EU.

- An online subscription business may add multiple acquirers to reduce involuntary churn when recurring transactions are declined by a single bank.

This diversification ensures that no single provider can become a bottleneck for revenue.

Why do merchants choose multiple acquirers?

The move to a multi-acquirer setup is driven by measurable benefits:

- Higher approval rates: Acquirers have different relationships with issuers. If Acquirer A rejects a payment, Acquirer B might approve it. This cascading effect can improve authorization rates by 5–15%, translating into millions in recovered revenue for large enterprises.

- Global reach: Local acquirers are often better connected to domestic issuing banks. For instance, approval rates in Brazil can be 20% higher when using a domestic acquirer versus a cross-border one.

- Cost optimization: Routing transactions to local acquirers helps merchants avoid costly cross-border or currency conversion fees. Over time, this can reduce payment costs by several percentage points.

- Business continuity: Outages happen. With multiple acquirers in place, merchants can reroute traffic instantly, protecting revenue during high-volume events such as Black Friday.

- Negotiation power: With multiple relationships, merchants can compare fee structures and leverage volume to negotiate better rates.

What are the challenges of managing multiple acquirers?

While the advantages are clear, managing multiple acquiring banks can be overwhelming without the right infrastructure.

- Integration overhead: Each acquirer requires a separate technical integration, certification, and ongoing maintenance. For engineering teams, this means duplicated work and higher costs.

- Data fragmentation: Each acquirer provides its own reports, making reconciliation a manual and error-prone process. Finance teams often struggle to close books on time due to scattered data.

- Routing complexity: Deciding which acquirer should handle which transaction requires real-time logic based on region, card network, or cost. Without automation, merchants often miss optimization opportunities.

- Compliance & risk management: Different acquirers may impose different fraud rules, PCI requirements, or regional compliance checks (PSD2 in Europe, LGPD in Brazil, etc.). Coordinating across them becomes resource-intensive.

- Operational inefficiency: Payment teams spend time firefighting issues—switching acquirers manually during outages, piecing together analytics from multiple dashboards—rather than focusing on strategy.

How can orchestration simplify acquirer management?

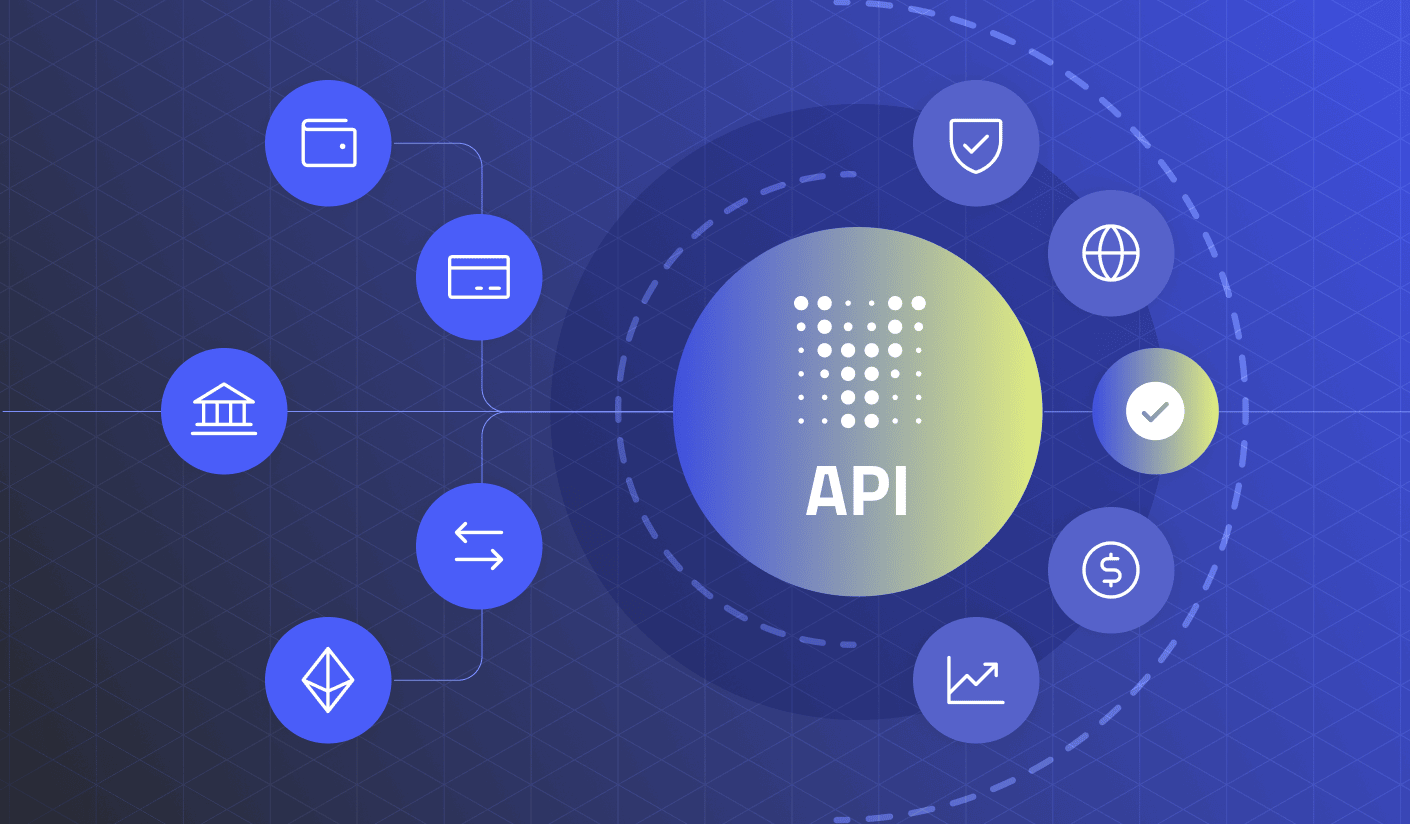

Payment orchestration platforms such as Yuno remove these barriers by consolidating all acquirers under a single integration.

With orchestration, merchants gain:

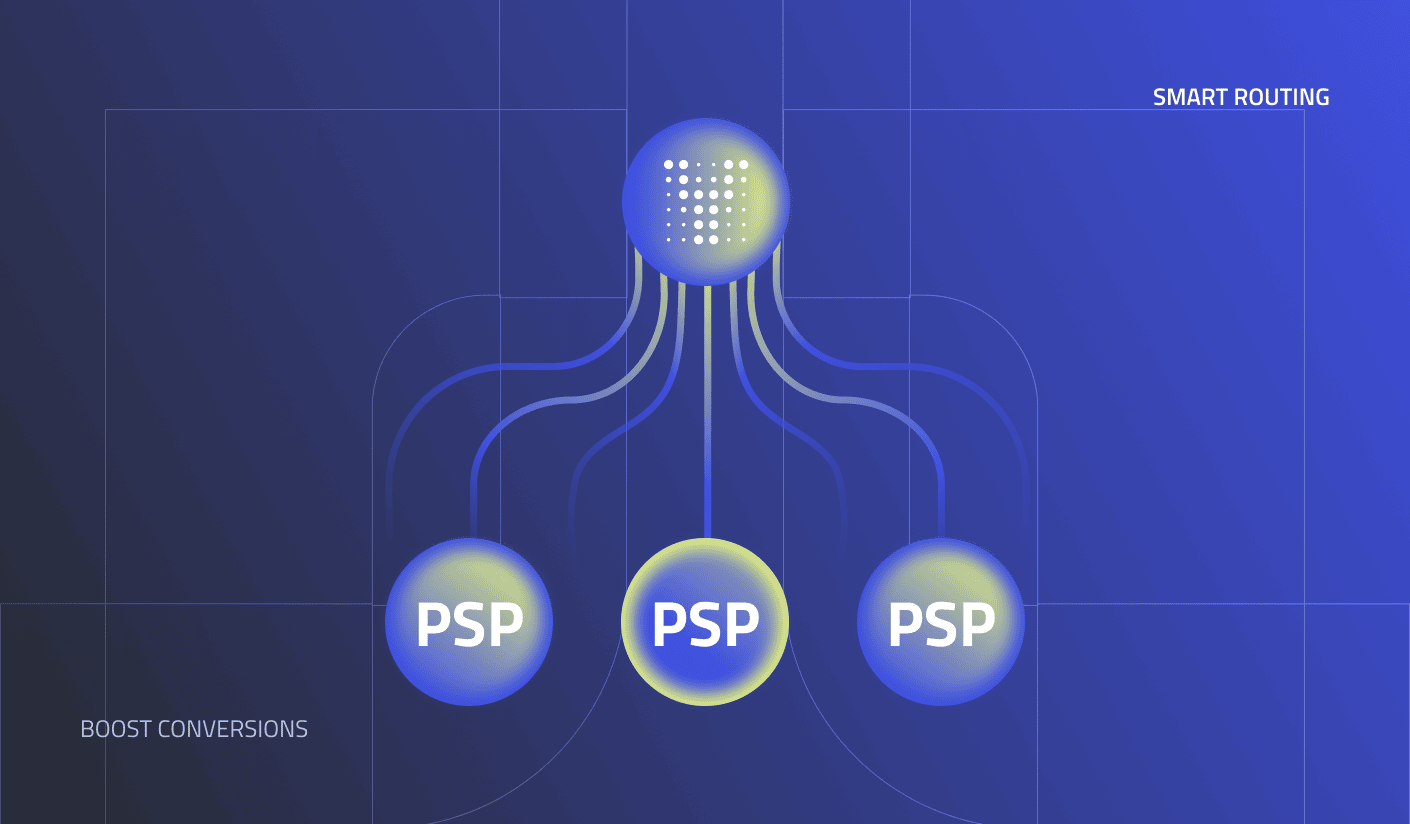

- Smart Routing: Transactions are directed to the best-performing acquirer in real time, based on KPIs like approval rate, cost, or latency.

- Fallback logic: If a payment fails with one acquirer, the platform automatically retries with another, recovering lost revenue without manual intervention.

- Unified reconciliation: All settlement and fee data flows into one dashboard, giving finance teams a single source of truth for reporting and audits.

- Fraud & compliance integration: Orchestration layers embed anti-fraud tools and regulatory checks consistently across all providers, simplifying compliance.

- Faster onboarding: Instead of months of integration, new acquirers can be added in days or even hours via pre-built connections.

This allows enterprises to act strategically with their payments instead of being trapped in operational complexity.

Merchants using Yuno typically see:

- 7–10% improvement in approval rates through optimized routing.

- Up to 30% reduction in transaction costs by leveraging local acquirers.

- Faster global expansion, with market entry timelines cut from months to weeks.

How do multiple acquirers improve global expansion?

Expanding internationally is one of the strongest cases for adopting a multi-acquirer strategy.

- Localized approval optimization: Domestic acquirers often achieve 10–20% higher approval rates compared to cross-border processing. For example, using a local acquirer in Mexico for card payments can significantly outperform routing those payments through a U.S. acquirer.

- Access to local methods: Many acquirers also connect merchants to popular regional methods like Pix in Brazil, UPI in India, or SEPA in Europe.

For a full breakdown of how payment method mix, approval benchmarks, and A2A rail adoption differ across LATAM, APAC, and MENA, see the Global Payment Infrastructure Playbook.

- Regulatory compliance: Local acquirers are better aligned with regional regulations, helping merchants avoid penalties or disruptions.

- Customer trust: Shoppers are more likely to complete payments when they see local acquirer names on their statements, which reduces chargebacks and builds confidence.

By combining these benefits, businesses can launch in new markets up to 3–5x faster with reduced costs and higher conversion.

What KPIs should merchants track in a multi-acquirer strategy?

To measure success, merchants should monitor a consistent set of metrics across all acquirers:

- Authorization/approval rate per acquirer: Identifies underperforming providers and highlights optimization opportunities.

- Transaction cost per region: Tracks interchange, scheme, and processing fees to ensure routing decisions maximize profitability.

- Fallback recovery rate: Quantifies how many declined transactions were successfully recovered via retries.

- Downtime & latency: Ensures business continuity by monitoring provider uptime and transaction response times.

- Chargeback & fraud ratio: Prevents higher approval rates from inadvertently leading to more disputes or fraud.

- Time-to-market: Measures how quickly new acquirers can be onboarded in different regions—a critical metric for fast-moving enterprises.

Industry examples of multi-acquirer strategies

- Subscription businesses: Streaming and SaaS companies often use multiple acquirers to reduce involuntary churn. For instance, if a monthly renewal fails with Acquirer A, it can be retried instantly with Acquirer B, preventing subscription cancellations.

- Marketplaces: Large platforms with sellers in different regions benefit from local acquirers for better conversion and compliance, while orchestration ensures centralized control.

- Retailers in emerging markets: Enterprises entering LATAM or APAC often adopt local acquirers early on to compete with domestic players who already provide trusted local payment experiences.

These examples demonstrate that a multi-acquirer approach is not just about redundancy—it is about aligning payments with business models and growth objectives.