What is digital payment processing?

.png)

When it comes to online transactions, everyone expects to pay as quickly and easily as they would handing over cash in a store. This is the essence of digital payment processing: replacing the need for physical cash or checks while enhancing speed, security, and convenience.

Digital payment processing refers to the technology and systems that facilitate electronic transactions between customers and businesses. Whether it’s paying for a coffee using a mobile wallet or completing a high-value cross-border transfer, these systems handle everything from authentication to fund transfers, ensuring transactions are smooth and secure.

Digital payment processing technology emerged to address the inefficiencies and risks of traditional payment methods. Cash transactions were slow and impractical for remote or large-scale purchases, while checks often caused delays and were vulnerable to fraud. Digital payment processing solved these issues, paving the way for a more streamlined and scalable commerce ecosystem.

Today, digital payments power everything from online shopping to peer-to-peer transfers, enabling businesses to meet modern consumer expectations. For example:

- A customer buys groceries online with a credit card processed through a secure payment gateway.

- A subscription service automatically bills customers monthly using a recurring payment system.

- A global business pays an international supplier, seamlessly handling currency conversion through digital payment technology.

As digital commerce continues to grow, mastering digital payment processing is critical for businesses looking to deliver better customer experiences and stay competitive, especially as cross-border transactions are projected to reach $290 trillion by 2030.

Exploring the types of digital payments

Digital payments have revolutionized the way commerce operates, offering businesses an ever-expanding range of options to meet diverse customer needs. Each method comes with its own advantages and challenges, making it important for businesses to choose the right mix.

Mobile wallets

Mobile wallets like Apple Pay and Google Pay provide a fast, secure way to process payments. They simplify the checkout process, reduce cart abandonment, and enhance customer satisfaction.

However, adopting mobile wallets requires businesses to have compatible technology infrastructure and seamless integrations with various providers. Failing to keep systems updated can lead to missed opportunities with wallet-preferred customers.

Buy now, pay later (BNPL)

BNPL solutions enable customers to split their payments into manageable installments, making high-ticket items more accessible. For merchants, this drives sales and attracts budget-conscious shoppers who might otherwise abandon their purchase.

That said, BNPL can present challenges, such as higher transaction fees and increased risks of defaults or returns. Merchants must carefully evaluate the cost-benefit balance of offering these solutions.

Electronic transfers

Electronic transfers are a cost-effective option for recurring payments or high-value transactions. They offer lower fees compared to many other methods, making them ideal for businesses focused on cost efficiency.

However, their slower processing times can pose challenges for businesses that require immediate fund confirmation, especially when compared to instant payment solutions.

How digital payment processing works

Digital payment processing relies on several key participants to complete a secure transaction. These include:

- Payer: The customer initiating the transaction.

- Payee: The business or merchant receiving the payment.

- Payment gateway: Facilitates the secure transfer of payment details.

- Payment processor: Acts as the intermediary, validating transaction details, transferring funds, and updating both parties on the payment’s status.

The four steps in digital payment processing

Benefits of digital payment processing for businesses

Digital payment processing empowers businesses with tools to enhance efficiency, reduce costs, and deliver better customer experiences.

Increased efficiency

By automating transaction workflows, digital payment systems eliminate manual processes, reducing errors and freeing up valuable time. Faster transaction speeds also allow businesses to serve more customers in less time, boosting overall productivity.

Cost savings

Digital payments often come with lower transaction fees compared to traditional methods like checks or wire transfers. Additionally, by reducing reliance on manual processes, businesses can cut operational costs and allocate resources more effectively.

Enhanced customer experience

Consumers today expect payment options that are fast, flexible, and seamless—whether that’s tapping a phone to pay, setting up recurring billing, or using BNPL services. Meeting these expectations builds loyalty and increases retention.

Competitive advantage

Adopting digital payments helps businesses stand out in competitive markets. Companies that fail to offer modern payment options risk losing customers to competitors that prioritize convenience and innovation.

Data-driven insights

Digital payment systems generate valuable data on customer behavior and spending patterns. Businesses can use these insights to optimize marketing strategies, tailor offerings, and foster stronger customer relationships.

Challenges in digital payment processing

Despite its many advantages, digital payment processing is not without challenges; businesses must address these issues to fully realize their potential.

Security risks

The rise of digital payments has also led to increased cyber threats. Hackers target payment platforms to steal sensitive customer data or commit fraud. A single breach can damage a business’s reputation and result in significant financial losses. To mitigate these risks, businesses must invest in robust security measures like encryption, tokenization, and fraud detection tools.

Regulatory compliance

Different regions have varying regulations on data privacy, consumer protection, and tax reporting. For businesses operating internationally, staying compliant can be complex and resource-intensive. Regular monitoring and adherence to evolving regulations are critical for success.

Technology barriers

Small businesses or those in regions with limited digital infrastructure often struggle to adopt advanced payment technologies. High setup costs and outdated systems can hinder growth. Strategic investments in infrastructure and partnerships with reliable payment providers can help overcome these barriers.

Simplifying digital payment processing with orchestration

Managing multiple payment methods, gateways, and compliance requirements can overwhelm businesses as they scale. Payment orchestration provides a streamlined solution, acting as a central hub that connects payment providers, fraud tools, and regulatory frameworks.

Payment orchestration platforms enable businesses to manage payments from a single dashboard, optimize transaction flows, and ensure compliance across regions. This simplifies operations, reduces costs, and delivers a seamless payment experience for customers.

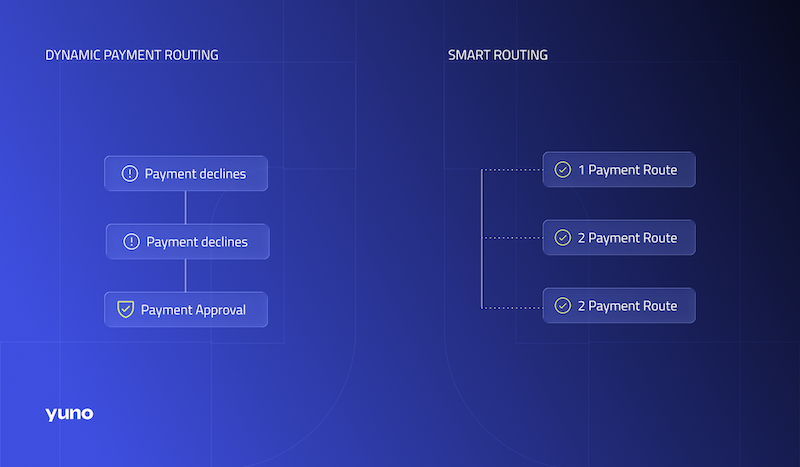

Yuno goes further by offering a unified platform that integrates over 300 payment methods, complete with features like smart routing, dynamic fraud prevention, and compliance automation. With Yuno, businesses can reduce operational complexity, enhance flexibility, and drive global growth.

Ready to simplify your payment strategy? Explore how Yuno’s payment orchestration platform can transform your operations and boost conversions.

More from the Blog

More from the Blog

Talk with one of our payment experts

Explore how Yuno's innovative payment orchestration solutions can help you increase approval rates, reduce costs, seamlessly integrate over 1,000 global and local payment methods, and simplify payment management.

Yuno is proudly certified to the highest industry standards, ensuring that data is handled with the utmost security and compliance. Its certifications include ISO 27001 and ISO 27701 for information security and privacy management, GDPR compliance for data protection, PCI DSS for secure payment processing, SOC 2 Type 2 for service organization controls, and recognition as a Visa Service provider. These certifications demonstrate Yuno's commitment to delivering trusted and secure services for businesses worldwide.

%20(1)%20(1).png)