Payment Tokenization in the U.S.: What It Is and Why It Matters

Fraud attempts continue to rise as commerce shifts online. Card testing and breaches become more severe when customer payment information is exposed to more systems. Every exposure point is a risk.

Security drives growth now. Customers expect saved cards and fast checkouts that work on any device. Risky transactions? They abandon. Data leaks? They leave.

Payment tokenization replaces card details with a token that has no value outside your payment flow. The token powers transactions and recurring billing without exposing the primary account number (PAN). You get stronger security and simpler PCI DSS compliance while checkout stays smooth.

Let’s break down payment tokenization and why it matters for your US operations.

What Payment Tokenization Is

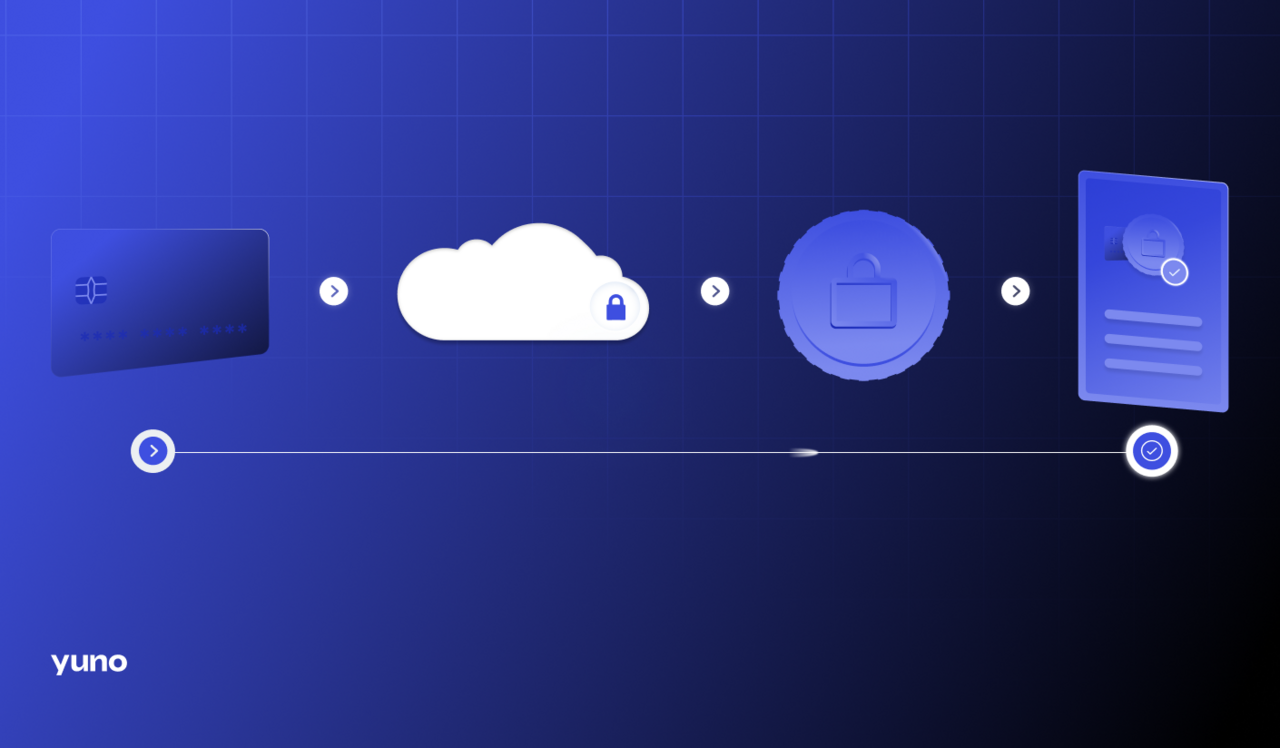

Tokenization swaps customer payment information for a random token. It replaces card details and the primary account number PAN with a value that has no meaning outside your system. The original data sits in a secure vault, while the token is what your systems store and use.

When a customer enters card details, a tokenization service issues the token. Your environment only sees the token, never the PAN. The token works for authorization and capture and powers future charges. The vault maps tokens to card data when needed, but your systems never hold clear PANs.

Token Types and Use Cases

Payment tokenization work varies by type. Different tokens solve different needs.

- Network tokens. Come from card networks like Visa and Mastercard. They tie to a specific card, merchant, and device. Use them for stored cards and subscriptions – they update automatically after card reissue. Network tokens receive strong issuer recognition and reduce data-breach risk by lowering fraud signals.

- PSP or gateway tokens. Come from payment service providers and tie to your merchant account with that provider. Use them for single-PSP setups and quick vaulting. Fast to implement and reduces the risk by cutting the PCI scope.

- Device tokens. Power wallets like Apple Pay and Google Pay. They bind to a device secure element for contactless and in-app card payments. Strong device security with minimal exposure.

- Merchant or orchestration tokens. Sit in your orchestration layer and enable multi-PSP routing and retries. They unify customer profiles and provide provider-agnostic flexibility while you retain ownership of stored credentials.

How Payment Tokenization Works

The Process – from Card to Token

A customer enters card details at checkout. A secure SDK or payment gateway sends card data to the tokenization service, which returns a token. Card data stores in a PCI-compliant vault. At the same time, your system uses the token to authorize and capture funds and power subscriptions or one-click returns.

What Payment Gateways Do

Payment gateways issue and manage tokens, handle vault mappings, and enforce PCI DSS controls. They process lifecycle events (such as card updates) using network tokens, reducing declines after reissue.

An orchestration platform can maintain merchant tokens across multiple gateways. That preserves your saved cards so customers don't need to re-enroll.

Tokens During Transactions

Tokens act like card stand-ins. During authorization, the payment processor maps the token to the PAN. Some benefits include:

- Security – PAN never touches your environment

- Continuity – tokens power retries, routing, and recurring billing

- Lower friction – saved payment methods and one-click are safer to support

Benefits in the U.S. Market

Security and Fraud Reduction

Tokens have no intrinsic value to attackers. They're useless outside their domain. Reducing PAN exposure reduces the attack surface. At the same time, network tokens improve issuer recognition, which can increase approvals and reduce fraud signals.

PCI DSS Compliance

Tokenization reduces PCI scope by removing card data from your systems. That simplifies audits, cuts assessment time, and lowers compliance costs. You still need controls where tokens live, but the most sensitive data sits in a hardened vault.

Customer Trust and Experience

Customers want speed and safety. Tokenization makes "save my card" and "buy again" effortless while network tokens handle card lifecycle updates. That cuts unnecessary declines when cards are replaced – fewer interruptions, higher conversion, more returning customers.

Challenges and Limits

Implementation Complexity

Tokenization introduces architectural decisions around gateway tokens, network tokens, merchant tokens, or a mix of them. Each affects routing flexibility, vendor lock-in, and operational overhead. Plan for migration paths and token portability from the start.

Token Governance Risks

Tokens still require strong controls. Poor key management, weak access controls, or sloppy vault operations expose you to risk and downtime. Choose partners with proven PCI DSS compliance and clear SLAs. Monitor token lifecycle, rotation, and detokenization paths.

Workflow Limits

Some workflows still need clear PAN access for disputes, regulatory checks, and deep fraud investigations. Ensure detokenization is controlled, auditable, and restricted to least-privilege users and systems.

The Future

Digital Wallets and Contactless

Device tokens enable contactless wallets such as Apple Pay and Google Pay. As NFC grows and in-app wallets expand, device-bound tokens will continue to enhance security tokenization across online and in-person channels.

AI and Emerging Tech

AI-driven fraud tools already analyze tokenized data to spot patterns and stop attacks faster. Expect smarter risk models that use token metadata while preserving privacy. Experts are exploring blockchain for auditable token maps, though mainstream adoption for payment processing is still early.

Regulatory Shifts

Watch evolving standards from the PCI Security Standards Council for token formats, lifecycle events, and interoperability. Broader network token adoption and harmonized policies will support safer, more consistent acceptance nationwide.

What to Do by Role

CFO: Reduce Loss, Stabilize Margin

Network tokens and issuer-trusted credentials cut unnecessary declines and related costs. Quantify PCI scope reduction – shifting PANs out cuts audit effort and budget. Model vendor lock-in risk by balancing near-term savings from PSP tokens against long-term flexibility from merchant or network tokens.

CPO / Head of Payments: Lift Conversion, Speed Market Entry

Standardize on a token strategy that survives provider changes. Merchant or network tokens keep you agile across gateways while enabling saved payment flows – across web, app, and in-store channels. Tokens should travel safely across channels with clear governance. Use tokens for smart retries and adaptive routing to improve approvals.

CCO / Risk Leaders: Improve Fraud and Compliance

Prefer network tokens for stored cards where possible. Issuer recognition helps reduce fraud and false declines. Tighten detokenization access, enforce least privilege, and maintain audit trails for sensitive workflows. Document how tokenization reduces risk and shrinks PCI scope, streamlining audits.

Product / Engineering: Build for Portability

Abstract token handling behind a stable service that keeps business logic clean and supports multiple providers. Plan for token migrations using tooling and provider support for mapping, bulk migration, and dual-run cutovers. Validate SDKs and vaults to ensure PCI DSS compliance, uptime SLAs, and clear incident response.

How Yuno Helps You Operationalize Tokenization

Unify Strategy Across Providers and Markets

Yuno connects you to 200+ providers through a single API and centralizes token management. You control stored credentials as you route each transaction to the best-performing acquirer. Faster market launches, fewer one-off integrations. Learn more about Yuno's approach to network tokenization.

Reduce Fraud with Adaptive Risk Scoring

Tokens are safer, but fraud evolves. Yuno's adaptive risk scoring pairs with tokenization to block high-risk attempts without hurting conversion. Manage rules in one place and apply them across channels and providers.

Simplify PCI Scope, Speed Compliance

Moving PAN handling to certified partners and using Yuno as your orchestration layer reduces the risk of data breaches, streamlines audits, and de-risks expansion. Standardize how tokens are issued, stored, and used across your stack.

Keep Optionality Without Breaking Customer Experience

Yuno's model is provider-agnostic. Add a new gateway or optimize routes – your saved cards still work. You keep continuity for subscriptions, one-click, and retries without new customer enrollments or card re-captures.

Implementation Roadmap

Step 1: Choose Token Types for Your Flows

- Stored cards and subscriptions: Favor network tokens for card lifecycle continuity and issuer trust.

- Single-PSP setups: PSP tokens deploy quickly, but consider future portability.

- Multi-PSP orchestration: Use merchant tokens to preserve saved cards across providers.

Step 2: Map Token Flows to Routes and Channels

Define how tokens move through web, app, and POS. Align retry logic, soft declines, and partial captures. Ensure detokenization occurs only at trusted points with strong audit controls.

Step 3: Integrate with Governance and Risk Controls

Pair tokenization with device signals, 3DS where needed, and velocity rules. Maintain least-privilege access, rotate credentials, and monitor vault performance and failover paths.

Step 4: Test, Migrate, Monitor

Pilot with a subset of transactions and use A/B routing to compare approval rates and checkout time. Plan managed migration for existing stored cards. Track KPIs: approval rate, chargeback rate, checkout duration, support tickets.

Step 5: Optimize Over Time

Adopt network tokens where issuer support is strongest. Expand routing strategies to reduce issuer-specific and region-specific declines. Monitor regulatory updates affecting token formats and lifecycle events in the U.S.

Common Pitfalls (and How to Avoid Them)

Locking into One Provider's Tokens

PSP tokens are convenient but can slow future changes. Keep your architecture open by using an orchestration layer that supports merchant and network tokens for portability.

Treating Tokenization as "Set It and Forget It"

The token lifecycle and vault performance require ongoing care. Monitor token issuance, vault uptime, and issuer acceptance with network tokens. Adjust as patterns shift.

Underestimating Internal Access Controls

Token misuse can happen inside your walls. Enforce strict RBAC, use short-lived credentials, and maintain comprehensive logging around detokenization and refunds.

Why Tokenization Matters Now

Tokenization protects card data, reduces the scope of compliance, and improves the customer experience. It reduces fraud risk and maintains high conversion rates, especially in the U.S., where wallets, network tokens, and issuer controls are advancing rapidly.

As digital payments embed into every product, tokenization becomes foundational – the backbone for saved cards, subscriptions, and cross-channel checkout. It's also the bridge to issuer-trusted credentials and smarter routing.

Stay Ahead with the Right Partner

Yuno helps you unify tokenization, reduce fraud with adaptive risk scoring, and route transactions across 200+ providers through a single API. Planning a token strategy or migration? Talk to our team. We'll map the path that lifts approvals, lowers risk, and preserves flexibility.

FAQ

What types of businesses benefit most from payment tokenization?

High-volume merchants with stored cards see immediate value: ecommerce retailers, marketplaces, subscription businesses, and mobile-first apps. Financial institutions and wallet providers also benefit from device-bound tokens and issuer-trusted credentials that reduce fraud and improve continuity.

Is payment tokenization legally required in the U.S.?

Tokenization isn't mandated by law, but PCI DSS requires strict controls for any environment that stores, processes, or transmits cardholder data. Tokenization helps remove PAN from your systems and can reduce PCI scope, effort, and cost.

How does payment tokenization compare to encryption?

Tokenization and encryption serve different roles. Tokenization replaces the PAN with a token that is not mathematically reversible. Only the vault or network can map it back. Encryption transforms data into a ciphertext that can be decrypted with the proper keys. Both are vital and often used together: encryption protects data in transit and at rest, while tokenization minimizes where PAN is stored and used.

Ready to strengthen security and lift approvals? Yuno helps you operationalize tokenization, reduce fraud with adaptive risk scoring, and route payments to 200+ providers through a single API. Let's build this together.

More from the Blog

More from the Blog

.png)

Talk with one of our payment experts

Explore how Yuno's innovative payment orchestration solutions can help you increase approval rates, reduce costs, seamlessly integrate over 1,000 global and local payment methods, and simplify payment management.

Yuno is proudly certified to the highest industry standards, ensuring that data is handled with the utmost security and compliance. Its certifications include ISO 27001 and ISO 27701 for information security and privacy management, GDPR compliance for data protection, PCI DSS for secure payment processing, SOC 2 Type 2 for service organization controls, and recognition as a Visa Service provider. These certifications demonstrate Yuno's commitment to delivering trusted and secure services for businesses worldwide.

%20(1)%20(1).png)