What Happens When You Let AI Analyze Your Payment Data?

One in five eCommerce orders fails globally, producing roughly $47 billion in annual revenue leakage (Optimus, 2026). Most heads of payments do not find out their approval rate dropped until they open a weekly report. By then, the damage is done. AI payment analytics changes this equation: it converts raw transaction data into real-time decisions, not retrospective summaries.

Key Takeaways

- AI payment analytics closes the gap between when a payment problem starts and when a payment team acts, reducing response time from hours to seconds.

- Yuno's platform data shows smart routing lifts authorization rates by an average of 8 percentage points across enterprise merchants.

- Rappi reduced analyst time spent on payment disruption resolution by 80% after deploying AI-powered monitoring through Yuno's Monitors product.

- Multi-PSP data is the raw material AI needs. Single-PSP setups systematically limit what AI can see and optimize.

- False declines cost merchants roughly three dollars in lost revenue for every one dollar in processing fees (Optimus, 2026), making proactive AI intervention more valuable than reactive reporting.

Why Payment Data Has Always Been Underused

Most payment teams are data-rich and insight-poor. Transaction logs flow in from a dozen providers, but interpreting them requires switching between dashboards, querying databases, and mapping rejection codes to root causes manually.

We have seen this pattern across enterprise merchants in retail, mobility, gaming, and online education. The bottleneck is rarely the data itself. It is the time required to make sense of it across multiple providers simultaneously.

A payment team managing 20 or more processors cannot manually track approval rate drift by provider, card brand, and geography in real time. So they do not. They review aggregated metrics on a lag and respond to problems that are already costing revenue.

This is not an operational failure. It is a structural one. The tools have not matched the complexity of modern multi-provider payment stacks until now.

What AI Payment Analytics Actually Does

AI payment analytics applies machine learning to transaction streams, identifying patterns, anomalies, and optimization opportunities faster than any analyst can. The output is not a chart. It is an action: a routing change, an alert, a recovery attempt.

There are three distinct functions where AI changes the payment operation fundamentally.

Real-Time Anomaly Detection

AI monitors approval rates, rejection codes, and provider performance continuously. When a PSP degrades, or a specific card brand starts declining at higher rates in one country, the system flags it and reroutes traffic before analysts open their laptops.

Yuno's Monitors product does exactly this. Merchants define custom thresholds by provider, country, currency, or card brand. When the system detects a breach, it alerts the right people and automatically shifts volume to healthier providers. No manual intervention needed.

Rappi, which manages payments across 400 cities and nine countries with more than 20 active processors, reduced the time analysts spent resolving payment disruptions by 80% after deploying this capability. The system identifies and reroutes around provider issues in milliseconds rather than waiting for a human to notice.

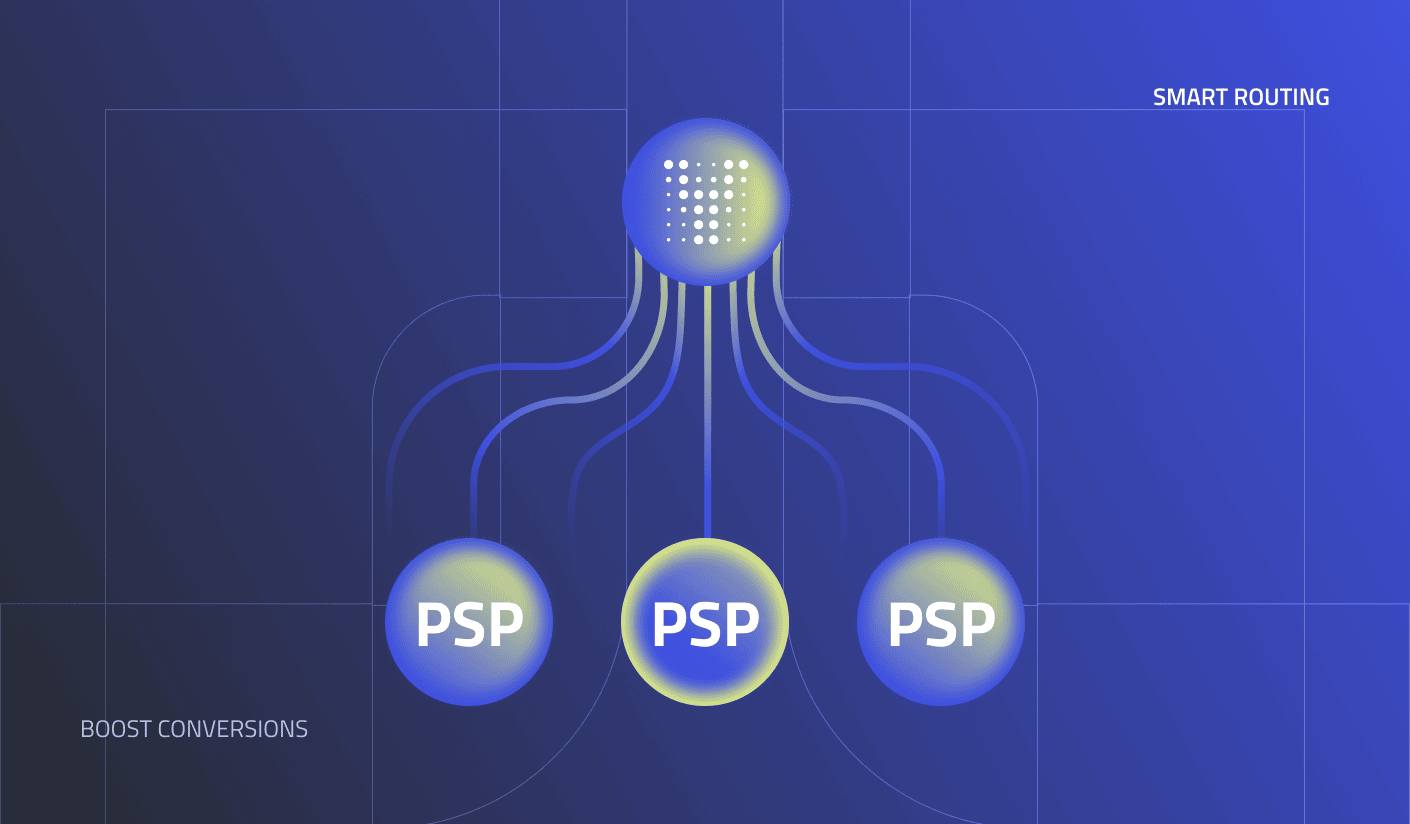

Intelligent Routing Recommendations

AI analyzes historical approval outcomes by PSP, card type, issuer, country, and transaction size to determine which provider is most likely to approve each specific transaction. It then routes accordingly.

This is not static rules-based routing. It adapts as PSP performance shifts, as card networks update their authorization logic, and as new rejection patterns emerge. Based on our infrastructure, merchants using smart routing see authorization rates lift by an average of 8 percentage points compared to fixed-routing setups.

The visibility required to make these recommendations is only possible with multi-PSP data. A single-provider setup cannot compare itself against alternatives. This is one reason Yuno's position as a neutral financial infrastructure platform matters: we route based on performance data, not on which provider we have a commercial relationship with.

Natural Language Querying Across the Payment Stack

Payment Concierge, Yuno's AI operations assistant, lets payment teams ask questions in plain language via Slack, WhatsApp, or the Payment Concierge interface and receive immediate, data-backed answers. No SQL, no pivot tables, no dashboard navigation required.

A head of payments can ask "Why did our approval rate drop in Germany yesterday?" and receive an answer with issuer-level rejection analysis and specific remediation steps in seconds. The same query without AI might require an analyst to pull data from multiple sources, cross-reference rejection codes, and report back hours later.

Payment Concierge can also generate Excel, PDF, or PowerPoint reports directly within the conversation. For payment leaders who spend significant time preparing executive briefings, this alone recovers hours per week.

How the Economics Change When AI Is Doing the Analysis

The revenue case for AI payment analytics rests on two numbers: the cost of inaction and the speed of intervention. Industry data shows merchants lose between 9 and 20% of annual revenue to payment failures (industry composite).

False declines make the problem worse. Merchants lose roughly three dollars in downstream revenue for every one dollar in processing fees when a legitimate transaction is declined (Optimus, 2026). AI routing reduces false declines by surfacing the PSP most likely to approve each transaction, rather than defaulting to a fixed provider order.

In our integrations across enterprise merchants in gaming, mobility, and marketplace verticals, the operational shift is consistent. Before AI monitoring, payment issues compound quietly. A provider degrades during a low-traffic window. Rejection rates climb. Customers abandon. The team discovers the problem at the next morning's standup. With AI monitoring, the same degradation triggers an alert and an automatic reroute within seconds of the threshold breach.

The revenue recovery compounds too. Yuno's NOVA product intercepts failed transactions and re-engages customers through WhatsApp or AI-powered voice in more than 70 languages, recovering up to 75% of contacted customers who would otherwise have churned. Viva Aerobus deployed NOVA and recovered more than $300 per transaction with zero manual effort and zero integration cost.

What Multi-PSP Data Makes Possible That Single-PSP Data Cannot

AI payment analytics is only as good as the data it can see. Single-PSP setups create a fundamental blind spot: the system cannot compare its own performance against alternatives.

With multi-PSP data flowing into a unified layer, AI can identify patterns that no individual provider can surface. Which processor outperforms for Visa transactions in India? Which one has a higher acceptance rate for UPI versus card rails? Which European acquirer handles iDEAL transactions more efficiently for a specific merchant category? These comparisons require data from all providers simultaneously.

inDrive, which operates across 50-plus countries, unified its payment infrastructure through Yuno and reached a 90% payment approval rate across markets. The routing intelligence behind that result depends on visibility across all active providers, not a single one.

Yuno's platform connects more than 1,000 payment methods across 200-plus countries through a single API. That breadth is what makes comparative AI analysis possible at scale. Payment Concierge can run side-by-side provider comparisons across regions, card types, and payment methods because it has access to the full multi-provider dataset, not a siloed slice of it.

Where AI Payment Analytics Is Heading in 2026 and Beyond

The frontier is shifting from reactive AI analysis to autonomous payment operations. AI is beginning to act, not just advise.

Generative AI traffic to U.S. retail sites grew 693% year-over-year during the 2025 holiday season (Adobe Digital Insights, January 2026). AI agents are not just analyzing payment data; they are initiating transactions on behalf of consumers. Gartner projects 20% of digital commerce transactions will be executed via AI platforms by 2030.

This changes what payment analytics must do. It is no longer enough to optimize the checkout experience for a human making a deliberate purchase. AI payment analytics must also support the infrastructure that processes transactions initiated by AI agents, where there is no human to re-enter card details or select an alternate payment method when the first attempt fails.

Yuno's Agentic Commerce product addresses this directly, making merchant catalogs purchasable inside ChatGPT, Claude, Gemini, and Perplexity through a single integration. The analytics layer underneath that commerce channel needs the same real-time monitoring, intelligent routing, and anomaly detection that enterprise payments require today.

The merchants who instrument their payment stack for AI analytics now will have a structural advantage when agentic commerce scales. They will already know which providers approve AI-initiated transactions at the highest rates, which markets need additional payment method coverage, and where their fallback routing holds up under pressure.

Three Practical Steps to Start Using AI for Payment Analytics

Getting value from AI payment analytics does not require a multi-year infrastructure project. The starting point is narrower than most payment leaders expect.

- Audit your rejection code distribution by PSP. Most payment teams look at overall approval rates. Drilling into rejection codes by provider reveals which PSPs are underperforming for specific card brands or geographies. This is the dataset AI needs to make routing recommendations.

- Define threshold alerts before problems occur. Set approval rate floors by provider and country. AI monitoring only prevents revenue loss if thresholds are configured in advance. Reactive threshold-setting after an incident misses the window entirely.

- Connect your AI analytics layer to where your team already works. Payment Concierge deploys via Slack, WhatsApp, or a dedicated interface. If payment insights require opening a separate tool, they will be checked less often. Meeting the team where they operate increases the speed of response.

The operational shift from retrospective dashboard review to real-time AI payment analytics is not primarily a technology question. It is a workflow question. The technology exists. The question is whether the payment stack is instrumented to surface the right signals and act on them fast enough to matter.

Start with the audit. The gaps in rejection code data by provider will show you exactly where AI has the most to offer.

More from the Blog

More from the Blog

Talk with one of our payment experts

Explore how Yuno's innovative payment orchestration solutions can help you increase approval rates, reduce costs, seamlessly integrate over 1,000 global and local payment methods, and simplify payment management.

Yuno is proudly certified to the highest industry standards, ensuring that data is handled with the utmost security and compliance. Its certifications include ISO 27001 and ISO 27701 for information security and privacy management, GDPR compliance for data protection, PCI DSS for secure payment processing, SOC 2 Type 2 for service organization controls, and recognition as a Visa Service provider. These certifications demonstrate Yuno's commitment to delivering trusted and secure services for businesses worldwide.

%20(1)%20(1).png)