Local or Invisible: Why 70% of GCC Shoppers Choose Local Payment Methods

Across the Gulf, digital payments have become the default. Yet for every frictionless Apple Pay tap, thousands of checkouts still fail silently - because the customer’s preferred local method isn’t available. In Saudi Arabia and the UAE, where mobile wallet penetration and domestic schemes dominate, missing these local-first options doesn’t just hurt user experience - it directly translates into millions of dollars in lost revenue.

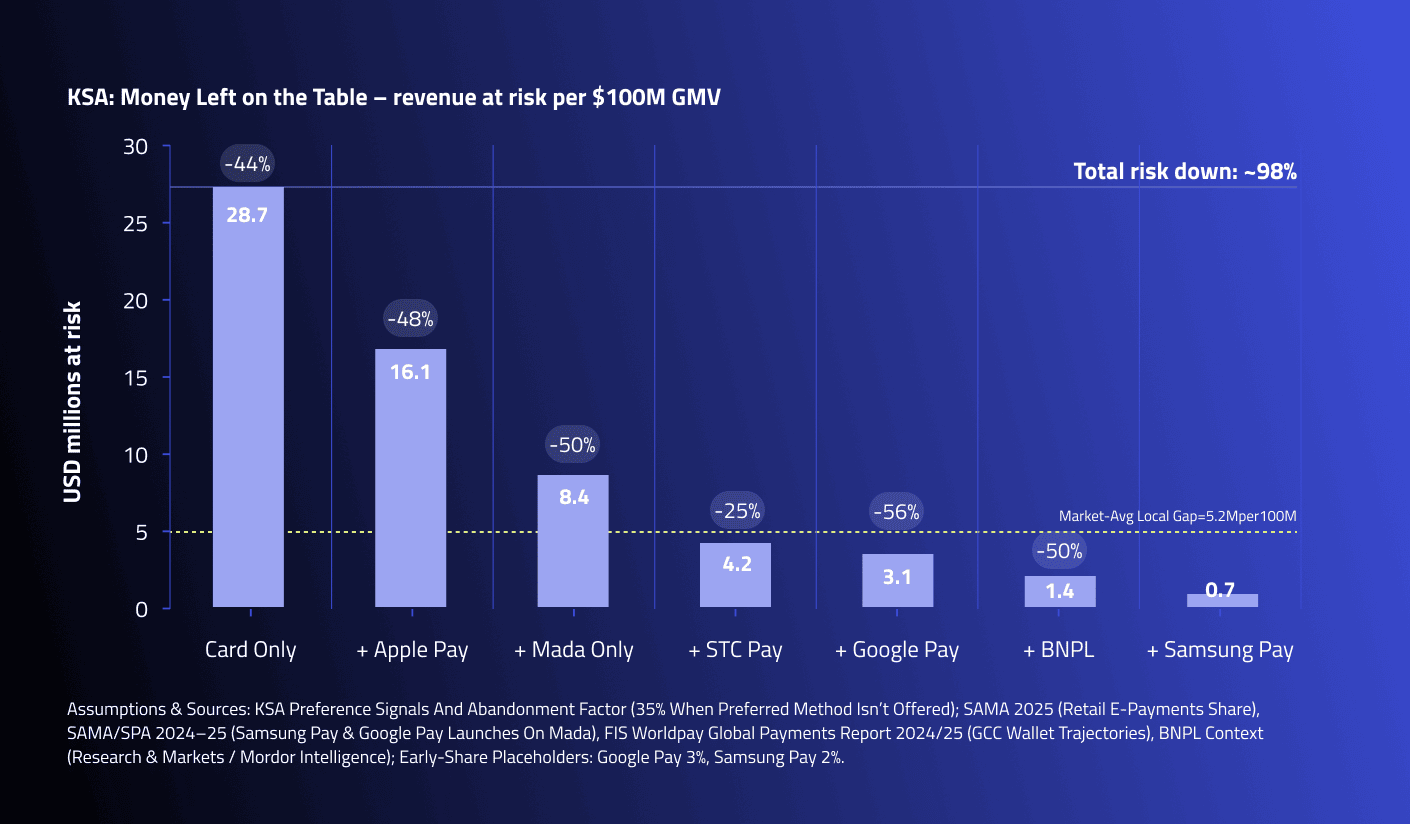

The $29 Million Problem: Revenue at Risk When Local Methods Are Missing

Every payment method missing from a checkout is a measurable loss. In Saudi Arabia, if an eCommerce business processes $100 million in online GMV, an estimated $28.7 million is structurally at risk when relying only on international cards.

Offering Apple Pay cuts that risk nearly in half. Add mada, and it drops again. Once STC Pay and BNPL are enabled, the “at-risk GMV” falls to just $2.5 million - a 90% reduction.

KSA: Missing local rails burns ~$5.3M per $100M GMV—turn on a full local-first mix to cut risk ~85–98%

This is not a UX optimization. It’s a P&L intervention. For every $100 million of GMV, failing to enable local-first methods can quietly erase 20–30 million in revenue opportunity.

The Coverage Gap: How Three Methods Capture 70% of KSA Shoppers

KSA’s digital payment shift is structural, not cyclical. According to recent consumer preference data, Apple Pay (36%), mada (22%), and STC Pay (12%) together account for nearly 70% of online checkout preferences.

Many enterprises expanding in GCC underestimate the cost of missing local rails.

The gap between what shoppers prefer and what checkouts offer translates into lost customers and revenue

When offered together, these three methods effectively “speak” to seven in ten KSA consumers in their first-choice payment language. In a market where 79% of all retail transactions are now electronic, these are not optional add-ons - they are the foundation of digital commerce.

UAE: A Preview of the Region’s Next Shift

While Saudi Arabia leads in domestic scheme adoption, the UAE showcases the next stage of wallet maturity. Apple Pay and Google Pay are near-ubiquitous, while BNPL providers like Tabby and Tamara are reshaping checkout expectations across fashion, travel, and electronics.

In Dubai alone, card-linked wallets and BNPL combined now cover over 60% of preferred eCommerce payments - a coverage ratio comparable to KSA’s local-first mix. The message for CFOs and Heads of Payments is clear: consumer preference across the GCC is converging toward wallet-first, local-first behavior, and merchants that fail to match that coverage risk structural underperformance.

Checkout Friction = Revenue Loss

When a customer can’t pay their way, they don’t switch payment methods - they switch retailers.

Globally, 35% of shoppers abandon their cart when their preferred method is unavailable, and in MENA, one in three will switch to a competitor after a single failed payment.

In high-growth Gulf markets, this dynamic compounds fast. A single payment failure can turn an $80 average order value into a lost lifetime customer. For enterprises managing hundreds of millions in annual GMV, even a two-point improvement in approval or conversion rate translates into millions recovered.

What “Best-in-Class” Looks Like in the GCC

In our analysis of 12 regional merchants, checkout conversion rates climbed from 1.4% to 2.6%+ as local-first coverage increased from one to five methods.

- Top quartile: Coverage ≥ 4 (Apple Pay, mada, STC Pay, BNPL) → Conversion ~ 2.3–2.8%.

- Median: Coverage 2–3 → Conversion ~ 1.7–2.1%.

- Bottom quartile: Coverage ≤ 1 → Conversion ~ 1.3–1.6%.

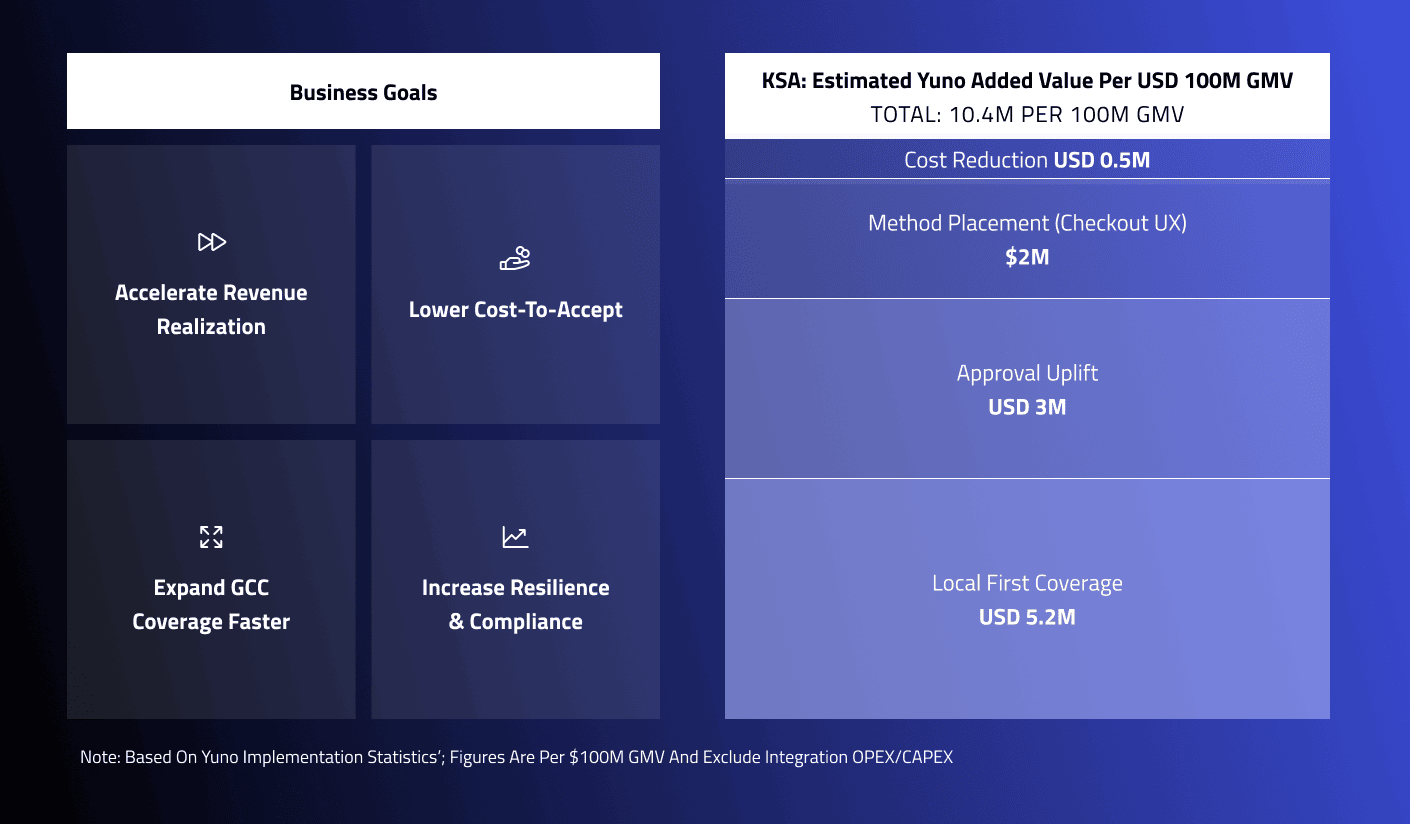

The Yuno Effect: Unlocking $10M per $100M GMV in Saudi Arabia

By bridging local payment rails and improving approvals, Yuno drives +7–10pp uplift in successful checkouts.

The pattern is consistent: as local-first coverage expands, conversion rates rise 8–12% above the median.

The Business Case for Local-First Enablement

The CFO lens turns preference data into financial materiality:

- $23 M GMV at risk per $100 M when 70% of preferred methods aren’t offered.

- 35% abandonment if the preferred method is missing.

- ~30% churn risk after a single failed payment.

The takeaway is direct: Payment method coverage isn’t a UX feature - it’s revenue protection.

How Yuno Enables Local-First Commerce Across the GCC

Yuno’s orchestration platform delivers instant access to all major GCC payment methods through a single integration - Apple Pay, mada, STC Pay, BNPL (Tabby/Tamara), KNET, BenefitPay, and more.

With Yuno, merchants can:

- Activate local-first methods fast: One API connection instead of multiple PSP contracts.

- Optimize approvals dynamically: Smart Routing automatically selects the highest-performing provider by issuer and method.

- Recover failed payments: Automated retries and fallback logic recover revenue lost to soft declines.

- Measure results: Real-time dashboards show approval rate uplift and GMV recovered by method.

The outcome: higher coverage, higher conversions, and a payment stack built for MENA’s wallet-first future.

Conclusion: From Coverage Gap to Competitive Edge

In 2025, being “local” no longer means translating a checkout - it means mirroring how your customers pay. GCC markets have made that expectation explicit: local-first is the language of trust.

Merchants that enable mada, STC Pay, and Apple Pay today aren’t just improving UX—they’re locking in future growth. For every $100 million in GMV, that’s $25–30 million that no longer leaks through the checkout.

In the GCC, the question is no longer whether local methods matter. It’s how fast you can orchestrate them.

More from the Blog

More from the Blog

%20(1)%20(1).png)

Talk with one of our payment experts

Explore how Yuno's innovative payment orchestration solutions can help you increase approval rates, reduce costs, seamlessly integrate over 1,000 global and local payment methods, and simplify payment management.

Yuno is proudly certified to the highest industry standards, ensuring that data is handled with the utmost security and compliance. Its certifications include ISO 27001 and ISO 27701 for information security and privacy management, GDPR compliance for data protection, PCI DSS for secure payment processing, SOC 2 Type 2 for service organization controls, and recognition as a Visa Service provider. These certifications demonstrate Yuno's commitment to delivering trusted and secure services for businesses worldwide.

%20(1)%20(1).png)